As the Puerto Rican economic and debt crisis deepens, one has to be struck by the partial solutions being advanced for its resolution. The Obama administration and Democratic senators put much faith in affording Puerto Rico with Chapter 9 bankruptcy protection akin to that currently enjoyed by all U.S. municipalities. For their part, Republican members of Congress put much store on the imposition of a mid-1990s New York City-style financial control board that would exert the budget discipline that the island has been so sorely lacking.

Yet neither of these proposals addresses the island's core issue, which is that it has been stuck in an economic slump over the past decade. Sadly, that slump now shows every sign of picking up pace.

As Greece's recent dismal economic experience attests, a declining economy tends to seriously exacerbate an economy's debt problem. The smaller the economy becomes, the less able it becomes to repay its debt. Puerto Rico would seem to be no exception to this rule, since a large part of its current inability to service its $72 billion debt mountain is the fact that its economy today is some 15 percent smaller than it was in 2005. Over the same period, the island has lost 10 percent of its population, with the exodus to the mainland picking up pace sharply in 2015 as Puerto Rico's financial crisis has deepened.

The reasons for Puerto Rico's economic slump are not difficult to identify. Manufacturing tax preferences for the island legislated by Congress, which had earlier encouraged investment and economic growth, were completely phased out by 2005. Over the same period, the island's public finances were grossly mismanaged. It also did not help that the U.S. military presence on the island was scaled down and that the island was subject to the same minimum-wage requirement as was the mainland. That minimum-wage requirement is reflected in a labor participation ratio of around 45 percent, which is more than 20 percentage points below the corresponding ratio on the mainland.

Against this background, it is difficult to see how either the imposition of a control board or the affording of Puerto Rico with Chapter 9 bankruptcy protection would in and of themselves place the island on a higher growth path. Indeed, one would expect that by imposing budget austerity on the island at the same time that it is locked in a monetary union with the United States that precludes it from following an independent monetary or exchange rate policy, its economic slump would deepen as it did in Greece. Similarly, while bankruptcy protection might spare the island from the debt-related legal free-for-all that would almost certainly otherwise occur in its absence, it is difficult to see how that protection in and of itself extricates the island from its current downward economic spiral.

Rather, it would seem that sorting out Puerto Rico's present economic and financial mess would require a comprehensive approach that emphasized policies to spur economic growth. A fiscal control board together with bankruptcy protection might certainly be helpful in that endeavor by exerting budget discipline and by avoiding a debt-related free-for-all in the courts. However, if Puerto Rico is truly to succeed, it would also need far-reaching structural economic reforms to get its economy growing again. As emphasized by the recent Krueger report, such reforms should include congressional action to modify Puerto Rico's minimum wage to make its economy more competitive, as well as amending the Jones Act to reduce the island's transport costs. Congress would also do well to reinstate manufacturing tax preferences for the island to encourage economic growth and investment.

As the litigation already started by bond insurers and the recent falling apart of the Puerto Rican electricity utility's debt restructuring deal remind us, the clock is ticking for Puerto Rico. Hopefully, House Speaker Paul Ryan (R-Wis.), who is promising to come up with a solution for the Puerto Rican crisis by the end of March, is hearing that clock. More important yet, hopefully, in coming up with a solution for the island, he will attach the highest priority to those measures that have the best chance of putting the island back on an economic growth path that might make it better able to repay its debts.

Lachman is a resident fellow at the American Enterprise Institute. He was formerly a deputy director in the International Monetary Fund’s Policy Development and Review Department and the chief emerging market economic strategist at Salomon Smith Barney.

Puerto Rico is pushing for a voluntary debt exchange deal with creditors as it struggles to manage a $72 billion public debt load that the governor has said is unpayable and needs restructuring.

Top officials in the U.S. territory's government held meetings Friday with creditors' advisers in New York to present the proposal, an official familiar with the matter told The Associated Press. The official was not authorized to talk to the media and agreed to confirm the sessions only if not quoted by name.

Gov. Alejandro Garcia Padilla declined to give details of the proposed deal. He reiterated a call for U.S. Congress to provide Puerto Rico with a debt-restructuring mechanism so it can avoid lawsuits as it tries to emerge from a nearly decade-long economic stagnation.

"Despite our good-faith efforts to find a common solution, it will be very hard to reach an agreement with multiple issuers without having access to a legal framework to implement the restructuring of our unsustainable debt," he said in a statement.

The meeting with the advisers comes just days before members of the U.S. House Subcommittee on Indian, Insular and Alaska Native Affairs hold a hearing to talk about creating an authority to oversee Puerto Rico's finances. Republicans have been pushing for a federal fiscal control board, but some Puerto Rico officials have rejected the idea of the federal government having such oversight.

Pedro Pierluisi, Puerto Rico's representative in Congress, has said he expects a legislative package to be unveiled after Tuesday's hearing.

President Barack Obama stressed the need for a comprehensive restructuring authority during a speech late Thursday at a U.S. House Democratic Issues Conference.

"(It) costs taxpayers nothing and will help more Americans regain control of their own economic security," he said.

Puerto Rico's government recently defaulted on $37 million in interest on bonds and has said it does not have the money to make upcoming payments, including a $400 million due in May. Three bond insurers have already filed lawsuits against the U.S. territory after it diverted funds to meet certain bond payments.

Sen. Elizabeth Warren is tying a long-brewing battle over the Puerto Rico financial crisis to an energy bill currently before the Senate.

The Massachusetts Democrat is offering an amendment to a wide-ranging energy reform bill from Sen. Lisa Murkowski (R-Alaska). Warren's proposal would help temporarily protect Puerto Rico from debt collectors until April 1.

Democratic Sens. Richard Blumenthal (Conn.), Kirsten Gillibrand (N.Y.) Bob Menendez (N.J.), Chris Murphy (Conn.), Bill Nelson (Fla.) and Charles Schumer (N.Y.) are backing Warren's amendment.

The senators argue that "a temporary stay on litigation is essential to facilitate an orderly process for stabalizing, evaluating, and comprehensively resolving" Puerto Rico's crisis.

A vote on the amendment hasn't been scheduled, but trying to link the two issues would place a deeply partisan fight into an otherwise uncontroversial energy bill.

Warren, Blumenthal, Schumer and Minority Leader Harry Reid (D-Nev.) introduced similar legislation last month, suggesting the temporary stay on creditor lawsuits would give Congress enough time to pass "comprehensive relief" for Puerto Rico.

Warren's latest move comes after every Senate Democrat united earlier this week to push Majority Leader Mitch McConnell (R-Ky.) to bring up legislation that would allow Puerto Rico to declare bankruptcy.

"If Congress doesn't act and give Puerto Rico the chance to restructure its debt, schools will shutter, utilities will be switched off, the sputtering economy will grind to a halt. It will be a nightmare, a nightmare," Schumer told reporters Wednesday.

Puerto Rican officials have been pushing lawmakers for months to take up legislation, with Democrats arguing that Congress accidentally withheld bankruptcy power from territories when it rewrote part of the U.S. code.

While Speaker Paul Ryan (R-Wis.) pledged that House lawmakers would work to come up with a solution by the end of March, how to solve Puerto Rico's financial crisis has divided senators.

A push by Schumer to pass legislation that gave Puerto Rico access to bankruptcy courts was blocked late last year by Sen. Orrin Hatch (R-Utah), who chairs the Finance Committee.

While both sides pledged to work together, Hatch suggested this week that huge policy and political gaps remain.

"I haven't heard much from the other side, but I'm prepared to work on it," he told reporters.

Hatch added that Democrats have focused on allowing Puerto Rico access to bankruptcy courts—a move he doesn't support.

Hatch, as well as Murkowski and Sen. Chuck Grassley (R-Iowa), have introduced alternative legislation. While it doesn't allow Puerto Rico to have access to bankruptcy courts, it would give the island territory up to $3 billion in federal assistance.

McConnell, who hasn't signed onto the GOP legislation, suggested that while lawmakers were broadly concerned about the Puerto Rico fiscal crisis, what Congress should do about it is unclear.

"We have a lot of discussion about what to do and as long as it doesn't involve the use of federal tax dollars, I think it is something we ought to try to figure out some way forward on," he told reporters on Wednesday. "Exactly what the way forward is at this point, I'm not sure."

Puerto Rico on Friday presented a plan to creditors that asks them to take a deep discount on their debt - an aggregate of around 45 percent, two sources familiar with the situation said, as the debt-ridden island tries to pull itself out of fiscal crisis.

With a 45 percent poverty rate and exodus of its population to the United States, Puerto Rico is trying to solve an economic crisis before substantial debt payments come due in May and July. The U.S. territory has defaulted on some of its debt and is trying to persuade creditors to take concessions.

Under the plan unveiled Friday, four tranches of bonds would be exchanged into two new bonds with different structures.

Haircuts on the debt would differ according to which bonds are being exchanged and would reflect the current trading of those bonds, the sources said, with general obligation bonds getting the best treatment, followed by COFINA bonds, subordinated COFINA bonds and then a slew of other bonds which are to be included in the offer.

The aggregate haircut across the structures would be around 45 percent, the sources said. Current trading of the bonds would indicate that general obligation debt would take a 30 percent haircut from the par value. General obligation bonds issued in 2014 are currently trading around 72 cents on the dollar.

The category of other bonds to be exchanged would include about a dozen issues, which include those supported by tax and legislative appropriations - such as bonds of highway authority HTA and infrastructure authority PRIFA and even PFC, which defaulted on its payments in August. It would exclude a handful of bonds including PREPA and aqueduct and sewer agency PRASA.

The plan may be greeted with skepticism by creditors, with one of the sources saying it was "uninviting" and noting it was premised on the island's financial projections, which some creditors believe are overly optimistic.

The newly-structured bonds would consist of a so-called 'base' bond and a 'hope' bond, the sources said, with the latter being a bet on the long-term health of the U.S. territory.

The base bond would start paying interest in 2018 at 2 percent, rising to 5 percent in 2021, when it would also pay principal, the sources said. It would have a general obligation guarantee and would receive pledged revenues to support the credit, one of the sources said.

There is a waterfall mechanism built into the offer which would give certain bonds a priority of payments depending on which tranche they are, the source said. The bonds which would be issued are expected to carry a roughly 5 percent yield, that source said.

The hope bond is a 30-year issue and would be based on a revenue formula with the aim of starting to pay out by 2026, the source said, with a cap on the payment for any given year. The territory could elect not to make a payment if unexpected budget costs come up. Some details of the bond exchanges were reported by The Wall Street Journal earlier.

If the territory fails to get a supermajority of creditors to agree to the exchange, it has the right to withdraw the offer, one of the sources said. That could spell a difficult scenario for creditors who may be left with illiquid bonds.

The plan is expected to be made public on Monday, the sources said.

The entire Senate Democratic caucus signed a letter Wednesday calling for Republicans to allow Puerto Rico to restructure its massive debt. But that show of unity masked divisions among Democrats as to what they would agree to as part of a negotiated solution to the island’s fiscal crisis.

Puerto Rico has some $72 billion in outstanding debt obligations, which Gov. Alejandro García Padilla has said cannot be paid. The island has already partially defaulted on some of its obligations, opting to pay higher priority creditors instead of bondholders with less solvent investments.

New York Sen. Chuck Schumer, the No. 3 Democrat in the Senate, struck a hard line on a solution Thursday, dismissing all options other than giving the island the ability to restructure its debts through Chapter 9 bankruptcy. “Without broad bankruptcy, you’re not going to solve Puerto Rico’s problems,” he said in an interview. “Broad bankruptcy doesn’t cost any money, and it does the most to solve the problem.”

Importantly, he also said transitional funds could not be used as an “alternative to bankruptcy.” Republicans have advocated for just that.

Asked whether he would consider any other possible restructuring options, such as a negotiated deal with Puerto Rico’s creditors, Schumer responded, “No. I’ve said what I’m going to say.”

The letter sent by Senate Democrats to Majority Leader Mitch McConnell (R-Ky.) advocated allowing Puerto Rico to use Chapter 9 bankruptcy, but it stopped short of endorsing it as the only possible restructuring option. It also noted that Puerto Rico had access to a bankruptcy option until 1984. Therefore, Democrats argue, it would not be unprecedented to restore that access.

Sen. Richard Blumenthal (D-Conn.), a member of the Senate Judiciary Committee, disagrees with Schumer’s Chapter 9-or-nothing approach. “There are other ways to restructure. Bankruptcy is just a vehicle to restructure,” Blumenthal said in an interview Thursday.

Blumenthal also said that transitional funds “may well be” necessary to prevent “chaos” in Puerto Rico in the near term. He opposes a Republican bill that would use $3 billion in funds from the Affordable Care Act to pay for the plan, but only because it raids Obamacare. “I would oppose that source of funds, but I’m open to alternatives that combine a restructuring of debt, whether through bankruptcy or other means, with longer-term relief,” he said.

Senate Republicans have all but ruled out allowing Puerto Rico access to Chapter 9 bankruptcy. McConnell said he is open to transitional assistance that doesn’t involve taxpayer money. On the specific question of bankruptcy, McConnell has deferred to the committees with jurisdiction over the law. Those leaders said they are opposed to changing the bankruptcy laws.

Allowing Puerto Rico access to Chapter 9 bankruptcy would not require the use of federal funds, but it would be a significant change to U.S. bankruptcy law. Creditors would also lose money, although they are unlikely to recoup the full value of their investments regardless of which solution lawmakers pick to address the island’s debt problem.

Senate Judiciary Committee Chairman Chuck Grassley (R-Iowa), whose panel has jurisdiction over the federal bankruptcy code, is not a fan of allowing bankruptcy for Puerto Rico. He has repeatedly said a solution to the commonwealth’s crisis must focus on other forms of restructuring and major reforms to its finances.

Along with Sens. Orrin Hatch (R-Utah) and Lisa Murkowski (R-Alaska), Grassley proposed legislation late last year that would provide some tax relief for island residents while imposing a financial control board to oversee the island’s financial restructuring. The bill also would provide $3 billion in transitional assistance funds.

Sen. David Perdue (R-Ga.), another member of the Judiciary Committee, said allowing Puerto Rico bankruptcy protection would be too much of a departure from the intent of the law.

“Chapter 9 was set up for municipalities. This is not a municipality. And we don’t make that available to states, so Puerto Rico doesn’t have that protection,” Perdue said in an interview Thursday. “They have to look at their asset sheet.”

Perdue suggested that the private sector might be willing to step in to provide transitional funds as part of a deal to privatize some inefficient public assets, such as the island’s electrical utility.

There remains no clear deadline for action in the Senate, and a spokesman for McConnell declined to comment on a timeline Wednesday. Speaker Paul Ryan (R-Wis.) wants the House to come up with a plan by the end of March.

There is emerging consensus on Puerto Rico's debt. It involves some form of a federal financial-control board, a legal structure for debt restructuring and somewhat better treatment of Puerto Rico on some federal programs. The concept that providing a mechanism for debt restructuring is a bailout is becoming discredited.

Initially, Anne Krueger, a consultant to the Puerto Rican government, advocated some form of debt restructuring. Later, she was joined by the likes of Nobel Prize-winner Joseph Stiglitz, economists from the Federal Reserve Board and economists from the U.S. Treasury Department. Lately, they have been joined by the likes of Desmond Lachman of the conservative think tank American Enterprise Institute, who published a column in The Hill favoring a legal framework for restructuring Puerto Rico debt.

Initially, mainstream media such as The New York Times published editorials advocating debt restructuring for Puerto Rico. Later, stalwarts from the financial media such as Bloomberg, joined in. Lately, the investor-friendly Wall Street Journal published an editorial favoring a legal mechanism for restructuring Puerto Rico's debt.

Bondholders tried to frame the discussion as one between themselves and the government of Puerto Rico as to which route was best for the well-being of Puerto Ricans. As of now, every significant segment of Puerto Rico's civil society is in favor of a legal framework for debt restructuring. This runs the gamut from religious leaders to local media and professional associations, to former Puerto Rico Gov. Luis Fortuño, who is a Republican. The few local Republican politicians who initially opposed debt restructuring have gone quiet.

Testimony before Congress by Puerto Ricans underlines the need for a legal framework to restructure debt. Richard Carrión, the chairman and CEO of Banco Popular, the largest commercial bank on the island, spoke not only about the need for a legal bankruptcy framework, but also his concern about Puerto Rico's pension liabilities. The government of Puerto Rico has already enacted legislation that resulted in most public sector employees enrolled in a defined contribution system with an employer matching contribution of zero. This is a more aggressive pension reform than the one declared unconstitutional in Illinois or the one imposed as part of the Detroit bankruptcy case.

The problem is that constitutionally, the Puerto Rican government cannot change the vested benefits of retirees or even present employees. When the pension funds run out of money in 2018, it will require some $800 million a year from the central government to pay the retirees. Proportionately to the U.S. economy, this would be the equivalent of an increase in government spending of $200 billion a year. Therefore, regardless of a federal financial-control board, government spending will have to increase unless the issue of vested pension benefits is examined as part of a debt-restructuring process.

Carlos Rivera recently testified before Congress on behalf of Puerto Rico's Private Sector Coalition, an umbrella organization comprising a wide range of private sector interests. In his testimony, Rivera spoke about the need for a legal bankruptcy framework for the island, and his concern about the preliminary debt-restructuring agreement with the Puerto Rico Electric Power Authority (PREPA).

PREPA is a government-owned corporation along the lines of the Tennessee Valley Authority. It is not part of Puerto Rico's central government budget. PREPA's equity position is negative $1.7 billion. Since it cannot file for bankruptcy, a preliminary agreement was reached that would provide some debt relief in exchange for significant rate increases to pay bondholders and perform necessary investments. While PREPA has been coy about how much the actual rate increase will be, the figure of 30 percent has been mentioned. This would be the equivalent of a tax of close to $1 billion a year on the people of Puerto Rico. The proportional figure for the U.S. economy would be somewhat around $240 billion annually. The comparison is not straightforward because, unlike Puerto Rico, the U.S. economy has not been contracting throughout the last decade and the U.S. is not losing population at a rate of almost 2 percent per year. Rivera's concerns are understandable.

Only two Puerto Ricans have testified in Congress against a legal framework for debt restructuring: a lawyer representing bondholders and an academic. Those opposing debt restructuring are an increasingly isolated group.

Feliciano is president of Advantage Business Consulting, which provides consulting services to the government of Puerto Rico on economic and tax policies, but not debt policy.

Carlos Gonzalez already had noticed the growing number of empty chairs and increasingly quiet slot machines at thePuerto Ricocasino where he worked as he mulled a job offer in theDominican Republic.

It was 2013, and Puerto Rico's economy had been in a downward slide for nearly a decade. Gonzalez didn't know it at the time, but the once-popular casino where he worked as a marketing manager would soon close.

He thought of his family and friends and the reasons he moved back to Puerto Rico in the first place after spending more than 20 years inNew Jersey. It took him several months to make a decision — "It's not easy to leave your land," the Puerto Rico native said — but he finally did.

"I never imagined it. Never!" Gonzalez said with a laugh. "I even asked myself 2,000 times whether I really was moving to the Dominican Republic. I told myself it was crazy."

The flow of migrants through the 80 miles (130 kilometers) of churning waters that separate Puerto Rico and the Dominican Republic has typically moved in one direction for more than half a century: toward the U.S. territory. But the island's deep economic crisis is reversing this trend, with a growing number of financially strapped Puerto Ricans moving to the neighboring Caribbean country to open businesses and escape economic chaos that has scared away even many Dominican migrants.

Officials say it's hard to quantify exactly how many Puerto Ricans have moved to the Dominican Republic in recent years because they fall under the general category of U.S. citizens, but they say the trend is undeniable.

"It used to be extremely rare for a Puerto Rican to stop by and seek a work visa," said Franklin Grullon, the Dominican consul in the Puerto Rican capital of San Juan. "There's been a surge in all types of visas, and we believe this flow will only increase."

The majority of Puerto Ricans seeking business visas are young to middle-aged men, and many request permission to work in the tourism sector because they speak English and find it easy to get a job, Grullon said. They are drawn by the Dominican Republic's robust economy, which grew 7 percent in 2015 for the second consecutive year, making it the strongest in the Latin American and Caribbean region. The government has credited vigorous performances in banking, construction and tourism, noting that a record 5.6 million tourists visited the Dominican Republic last year.

There's also been a big increase in Puerto Rican professionals such as architects and engineers traveling to the Dominican Republic to work because of that country's booming construction sector, said German Monroig, executive director of the office of Puerto Rican affairs.

"There's been a considerable change in the last two years," he said.

It's hard for Puerto Rican professionals to find steady jobs given the island's economy, which has stagnated for nine years as the U.S. territory of 3.5 million people struggles with a 12 percent unemployment rate and a $72 billion public debt load the governor has said is unpayable and needs restructuring. About a third of people born in Puerto Rico now live on the U.S. mainland, seeking to escape tax increases, higher utility bills and dwindling job opportunities.

"Puerto Rico became very, very difficult for the casino sector," the 48-year-old Gonzalez said. "I left just in time. ... All my friends tell me that the best thing I did was to leave, that Puerto Rico's situation is crazy."

Puerto Ricans aren't the only ones leaving.

Grullon said Dominicans are increasingly moving back to their country, and he noted that the flow of Dominicans entering the U.S. territory illegally also has decreased dramatically: The U.S. Coast Guard detained 1,565 Dominicans in 2004, compared with 133 in 2014.

"What's surprising about this trend is that up until now, the migration had been from the Dominican Republic to Puerto Rico, and the main motive was a difference in salary and more jobs," said Jorge Duany, an anthropology professor at Florida International University who has long studied migration patterns between the two.

In the early 1900s, Puerto Ricans were moving to the Dominican Republic to work in the country's thriving sugar industry until the Great Depression hit. Then Dominican migrants began moving to Puerto Rico in the 1960s and 70s because of the island's booming industrial sector. Roughly 200,000 Dominicans are now estimated to live in the U.S. territory, though there are no precise figures because many live on the island illegally.

Now, it's the lure of more jobs and a powerful economy in the Dominican Republic that is attracting Puerto Ricans, including 51-year-old Francisco Perez.

He worked more than 20 years for an insurance company in Puerto Rico, but began to see his income shrink as car sales on the island plummeted. When a job opportunity presented itself in late 2014 to work for a Puerto Rican company in the Dominican Republic that paid in U.S. dollars, he took it.

"I told myself I had to do what I had to do given the importance I have as my family's provider," said the father of four. "When I got here and saw that it was like Puerto Rico back in the 90s, that the economy was doing well, I stayed. I know there are a lot of Puerto Ricans looking over this way to grow their businesses."

Among them is Gonzalez.

He originally moved to the Dominican Republic to work as a marketing manager for a Hard Rock Cafe in the popular beach resort of Punta Cana, but he quit nearly two months ago to open his own tour company there.

"We're at full blast," he said, noting that he already has several contracts with large hotels in the region. "This is on the up and up."

A deal to restructure Puerto Rico’s troubled power utility’s $8.2 billion bond debt fell apart early yesterday, after lawmakers missed a Friday midnight deadline to approve key conditions for the proposed bond swap, including putting a debt payment charge directly on customers’ bills.

The agreement reached with 70 percent of the Puerto Rico Electric Power Authority’s bondholders would have cut its debt by $600 million and relaxed terms on more than $700 million in debt payments in return for the more secure new bonds. Officials warn the utility will run out of cash by summer without debt restructuring, possibly prompting power cuts.

Bondholders offered to extend the legislative deadline, but wanted to change terms of a $115 million loan that would have provided liquidity to PREPA, but the authority found the new conditions unacceptable.

“We are disappointed that the (bondholder) group did not grant our requested extension. PREPA remains willing to continue discussions,” said the authority’s chief restructuring officer, Lisa Donahue. She said bond insurers and bank lenders agreed to the extension without changing terms of the loan.

Representatives of the bondholders issued a statement describing the authority’s stance as “extremely disappointing and perplexing,” adding, “We continue to remain open to reaching a deal with PREPA and it is our sincere hope that they reconsider their position and assume postures beneficial to the people of Puerto Rico.”

Bondholders and PREPA officials said they expected lawmakers to approve the legislation in the next few weeks.

Officials have pointed to the power utility deal as a model for other debt-restructuring negotiations as Puerto Rico seeks relief from creditors who hold nearly $72 billion of debt across 18 different indebted government entities. Gov. Alejandro Garcia Padilla announced last June that the commonwealth could not pay its debt in the midst of a decade-long economic slide.

AP photo

NO DEAL: Lisa Donahue, the chief restructuring officer of the Puerto Rico Electric Power Authority, speaks with Jorge San Miguel, chairman of Environmental Law, Energy & Land Use, during Capitol Hill testimony on Jan. 12

The Association of Financial Guaranty Insurers (AFGI) said on Friday that granting bankruptcy protections to the government of Puerto Rico, which is struggling to pay its debts, would jeopardize its ability to reach a consensual debt restructuring.

In a letter to U.S. House of Representatives Speaker Paul Ryan, the association said it applauded U.S. Treasury Secretary Jack Lew's urging legislation outlining strong financial oversight for the Commonwealth to implement fiscal and economic reforms.

While pointing out that Lew did not explicitly join Puerto Rico's call for bankruptcy protection, AFGI said: "We remain concerned with any federal legislation that would authorize, or incentivize Puerto Rico to pursue nonconsensual restructuring of bonds issued by Puerto Rico or its public corporations."

Lew was in Puerto Rico on Wednesday to meet with the island's governor, Alejandro Garcia Padilla, as well as business and labor leaders. He again urged the U.S. Congress to pass legislation by the end of March to help the island handle its roughly $70 billion debt load.

Puerto Rico has begun to default on some of its bond issues and is negotiating with creditors to restructure its borrowings, but is facing a lawsuit from bond insurers who backed its debt.

(Reporting By Daniel Bases and Megan Davies; Editing by Nick Zieminski)

Rep. Debbie Wasserman Schultz pledged Friday to launch a renewed push for legislation that would provide a partial bailout for Puerto Rico’s $72 million debt, part of an economic crisis that has prompted tens of thousands of island residents to flee to Florida and other states.

Wasserman Schultz, a Florida representative who is also chairwoman of the Democratic National Committee, made the promise in response to a plea from Roberto Prats, a Puerto Rican lawyer, during a conference call with other DNC leaders.

Wasserman Schultz said she would help pressure House Speaker Paul Ryan, R-Wis., to act on a bill to restructure Puerto Rico’s debt and give the U.S. territory other financial relief.

“I want you to know how committed House Democrats are to making sure we hold the speaker’s feet to the fire and to making sure that by the end of March we pass legislation to help Puerto Rico,” the sixth-term lawmaker from Weston told Prats.

Ryan and other GOP leaders in the House and Senate have shown little willingness to aid the island, a majority of whose voters are Democrats. As residents of an American territory, they can vote in presidential primaries but not in the general election. Like the District of Columbia and other U.S. territories, Puerto Rico elects an at-large delegate to Congress who can craft and sponsor legislation, hold committee seats and perform other functions, but cannot participate in roll-call votes.

More than 1 million Puerto Ricans live in Florida, making them the state’s largest ethnic group after Cubans and forming the biggest Puerto Rican community in the United States outside New York.

Puerto Rico’s swollen debt, driven by benefits for the rising number of jobless residents and by other increased welfare payments, has prompted nearly 300,000 people to leave the island since 2012, with tens of thousands moving to Florida.

A measure to help Puerto Rico, crafted by Rep. Pedro R. Pierluisi, Puerto Rico’s congressional delegate, has languished before a House subcommittee since its introduction last February.

The bill has 37 co-sponsors, all, like Pierluisi, Democrats. Five House members from Florida – Wasserman Schultz, Ted Deutch, Alan Grayson, Patrick Murphy and Lois Frankel – are among the supporters.

In August, Puerto Rico paid only $628,000 on a $58 million debt bill, defaulting for the first time in the commonwealth’s history and sending shock waves through Wall Street. Much of its debt is held by American banks and other institutional bondholders.

Thirty-four U.S. hedge-fund managers are pressing for Puerto Rico to follow the conclusions of a study, released last June by former International Monetary Fund economists, that blamed the debt crisis on spending on public education and recommending that Puerto Rico close schools and fire teachers. It also proposed other spending cuts as part of broader austerity measures.

The report drew a sharp rebuke from Luis Gallardo, a city council member from Aguas Buenas, a town of 28,000 in Puerto Rico’s central mountains.

“These (type of) proposals have been a disaster for Latin America and would be so for Puerto Rico,” he said. “Sure, Puerto Rico could pay its debt, but at what cost? We are literally cutting off our own limbs just to stay afloat.”

During a visit Wednesday to the Puerto Rican capital of San Juan, Treasury Secretary Jacob Lew urged Congress to pass the legislation.

“The people of Puerto Rico are sacrificing, but unless that sacrifice is shared by creditors in an orderly restructuring, there is no path out of insolvency and back to growth,” Lew said.

Retired U.S. Bankruptcy Judge Steven Rhodes, who in November 2014 approved a mammoth Detroit settlement in the largest municipal bankruptcy in American history, is advising the Puerto Rican government on handling its crisis.

Among Republican presidential candidates, the Puerto Rican debt-relief bill has divided Sen. Marco Rubio of Florida and former Gov. Jeb Bush.

In a Spanish-language interview last July with Telemundo, Bush said the Detroit settlement could serve as a model for Puerto Rico but that Congress must intervene, because, unlike Detroit, the island does not have full legal jurisdiction to act on its own.

U.S. territory defaulted in August on debt payment for first time

With almost 1 million Puerto Ricans in their state, Florida lawmakers push for relief

GOP presidential candidates Jeb Bush and Marco Rubio split on bailout

Rep. Debbie Wasserman Schultz, a Florida Democrat, promised to press for Congress to consider a bill to partially bail out Puerto Rico from its debt. Puerto Ricans make up the second largest ethnic group in Florida, after Cuban-Americans. Steve CannonAP

i

Rep. Debbie Wasserman Schultz, a Florida Democrat, promised to press for Congress to consider a bill to partially bail out Puerto Rico from its debt. Puerto Ricans make up the second largest ethnic group in Florida, after Cuban-Americans. Steve CannonAP

Read more here: http://www.star-telegram.com/news/nation-world/national/article56156885.html#storylink=cpy

U.S. Treasury Secretary Jack Lew paid a visit to Puerto Rico, where he held a press conference urging Congress to take action to help alleviate the island's massive debt and humanitarian crisis.

During his first trip to the Caribbean island, Lew met with Puerto Rican officials on Wednesday to discuss ways to tackle the commonwealth's $72 billion debt.

"Only Congress can enact the legislative measures necessary for Puerto Rico to resolve this problem," he said at a news conference in San Juan. "The people of Puerto Rico are sacrificing, but unless that sacrifice is shared by creditors in an orderly restructuring, there is no path out of insolvency and back to growth."

Lew also laid out President Barack Obama's proposal to handle the crisis, which includes granting Puerto Rico's cities the ability to file for Chapter 9 bankruptcy, while providing the island with independent fiscal oversight, additional health care funding and employment incentives.

Republicans, however, have stalled on drafting a bill, arguing that they need more information about the island's financial situation. Others reject the idea of granting Puerto Rico restructuring powers because that would change the rules under which the debt was issued, they say.

Still, Lew stressed that "without congressional action, Puerto Rico will face a long and difficult recovery that could have harmful consequences for the American citizens who call the island home. That is why we have called on Congress to act without delay."

During the conference, Lew also mentioned that the U.S. territory is already defaulting on loans and struggling to balance funds between multiple creditors. Plus, the government has stopped some debt payments, leaving residents to carry the load wrought by the financial crisis.

"As predicted, creditors are filing lawsuits. Liquidity at the Government Development Bank, which provides essential banking and fiscal services to the central government, is low," he said, according to NBC News. "Tax refunds are being withheld and assets in the pension system have been sold to pay out pension bills."

Back in the States, House Speaker Paul Ryan, R-Wisc., has promised to work to reach a solution for Puerto Rico by the end of the quarter.

"Ryan has committed to producing a responsible solution for Puerto Rico before the end of March," his office stated in a press statement sent to Latin Post. "In order to assist the 3.5 million Americans who call this island home, Congress must pass legislation for the president to sign into law without delay."

Meanwhile, the Hispanic National Bar Association (HNBA) launched a task force on Puerto Rico, which will conduct a 10-week review to study the crisis and make recommendations on how the White House and Congress can help resolve it.

"Millions of families in Puerto Rico cannot continue to suffer the inaction of our federal government," HNBA President Robert T. Maldonado said in a statement to Latin Post. "In response to this lack of action, we have convened this Task Force to provide a thorough analysis and set of proposals to address the increasingly worsening economic situation on the island."

Resident Commissioner Pedro Pierluisi released the following statement regarding today’s announcement, by the Subcommittee on Indian, Insular and Alaska Native Affairs of the House Natural Resources Committee, that it will hold a hearing on Tuesday, January 26th at 11:00 a.m. entitled “The Need for the Establishment of a Puerto Rico Financial Stability and Economic Growth Authority”:

“I am pleased that House Natural Resources Committee Chairman Rob Bishop and Indian, Insular and Alaska Native Affairs Subcommittee Chairman Don Young have decided to schedule this hearing, which follows a hearing that another subcommittee of the Natural Resources Committee held last week on energy challenges and opportunities in the U.S. territory. In June 2015, the Subcommittee on Insular Affairs—of which I am a member—held a hearing that explored the causal relationship between Puerto Rico’s unequal and undignified status as a territory and its economic, fiscal and demographic crisis.

“I expect that, following next week’s hearing, a legislative package for Puerto Rico is likely to be unveiled. Let me be crystal clear. If this package seeks to impose a federal board to oversee the Puerto Rico government’s fiscal practices, but does not provide Puerto Rico with the authority to restructure a significant portion of its debt—as every state is authorized to do—or provide Puerto Rico with fair treatment under federal programs, I will adamantly oppose such an unbalanced package and it will not become law. I am willing to support a package that provides meaningful federal oversight of the Puerto Rico government’s fiscal practices, but only if it is paired with better—that is, more state-like—treatment of Puerto Rico.

“Over the years, Congress has a history of trying to provide Puerto Rico with ‘special’ treatment, and these efforts—whether well-intentioned or ill-intentioned—almost always end up harming Puerto Rico. My constituents are not laboratory rats upon whom the federal government should be undertaking policy experiments. Equality is the best policy.”

The Need for the Establishment of a Puerto Rico Financial Stability and Economic Growth Authority Tuesday, January 26, 2016 11:00 AM Subcommittee Indian, Insular and Alaska Native Affairs 1334 Longworth House Office Building, Washington, D.C. 20515

As a result of the efforts of Resident Commissioner Pedro Pierluisi, the Centers for Medicare and Medicaid Services (CMS) informed hospitals in Puerto Rico that they will soon begin receiving the same basic reimbursement rate—known as the “base rate”—as hospitals in the states for treating Medicare patients. This is because the Consolidated Appropriations Act for Fiscal Year 2016, enacted in December 2015, included the language of H.R. 1417, the Puerto Rico Hospital Medicare Reimbursement Equity Act, which Pierluisi introduced in March 2015.

For the first time in the history of the Medicare program, which was established in 1965, Puerto Rico hospitals will essentially be treated the same as hospitals in the states with respect to how they are reimbursed for the services they provide.

The Congressional Budget Office (CBO) estimates that, as a result of this legislative change, Puerto Rico hospitals will receive $618 million more in federal reimbursement payments between 2016 and 2025, an average of over $60 million per year. The Consolidated Appropriations Act also included the language of H.R. 1225, the Puerto Rico Hospital HITECH Amendments, a bill that Pierluisi introduced in order to make Puerto Rico hospitals eligible for the same bonus payments as hospitals in the states for adopting use of electronic health records. CBO estimates that this legislative fix will increase payments to Puerto Rico hospitals by $266 million over the next 10 years.

“On Thursday, CMS notified me it has informed Puerto Rico hospitals that increases in their reimbursement rates are forthcoming. Although it will take several months for CMS to fully implement these changes, which require updates to the agency’s computer systems, the changes will be made retroactive to January 1, 2016—so that Puerto Rico hospitals will receive the higher reimbursement rates for all Medicare patients who are admitted on or after that date,” said Pierluisi.

“Puerto Rico’s hospitals—and the patients they serve—deserve to be treated the same as hospitals in the states, and I am gratified that CMS is implementing the provisions of the Consolidated Appropriations Act that provide equitable treatment to our hospitals and our patients. There is still much work to be done to improve Puerto Rico’s treatment under Medicaid and Medicare, but it is important to acknowledge our accomplishments in this area when they do occur,” added the Resident Commissioner.

The Supreme Court on Wednesday raised doubts about whether Puerto Rico should be treated as a sovereign state with powers that go beyond its status as a territory of the United States.

The justices considered the question during arguments in a criminal case involving two men who claim that Puerto Rico and the federal government can't prosecute them for the same charges of selling weapons without a permit.

The double jeopardy principal prevents defendants from being tried twice for the same offense. But there is an exception that allows prosecution under similar state and federal laws, since states are considered separate sovereigns.

Several justices said Puerto Rico's power to enforce local laws really comes from Congress, which in theory could take it away.

The case has broad political and legal implications that could affect Puerto Rico on issues ranging from taxation and bankruptcy to federal benefits. It comes as the high court prepares to hear a separate dispute later this year over whether the financially struggling Puerto Rican government can give its municipalities the power to declare bankruptcy.

The Caribbean island of 3.5 million people is a U.S. territory acquired in 1898 following the Spanish-American War. But it gained a measure of autonomy in 1952, when it adopted its own constitution with the approval of Congress and was allowed to pass its own local laws.

Justice Elena Kagan said that history means the ultimate source of the island's legal power is Congress.

"If Congress is in the driver's seat, why isn't Congress the sole source of authority?" she asked Christopher Landau, the lawyer representing Puerto Rico.

Landau said that under Puerto Rico's constitution "the political power of the commonwealth emanates from the people." He said Congress had essentially relinquished control over Puerto Rico's internal affairs when it allowed the island to create its own laws and government.

But Justice Antonin Scalia said that doesn't mean Congress couldn't change the law.

Justice Sonia Sotomayor, the daughter of Puerto Rico-born parents, seemed sympathetic to the argument that Congress meant to confer sovereignty when it approved the island's constitution — even if Puerto Rico is not quite equivalent to a state.

"Before 1952, Congress could veto Puerto Rico's laws," Sotomayor said. "It has relinquished that right."

The case involves Luis Sanchez Valle and James Gomez Vazquez, who pleaded guilty in federal court to selling illegal firearms. When Puerto Rican officials later charged them under local laws, they moved to dismiss the charges on double jeopardy grounds.

The Puerto Rico Supreme Court ultimately sided with the men, ruling that the island is not a separate sovereign.

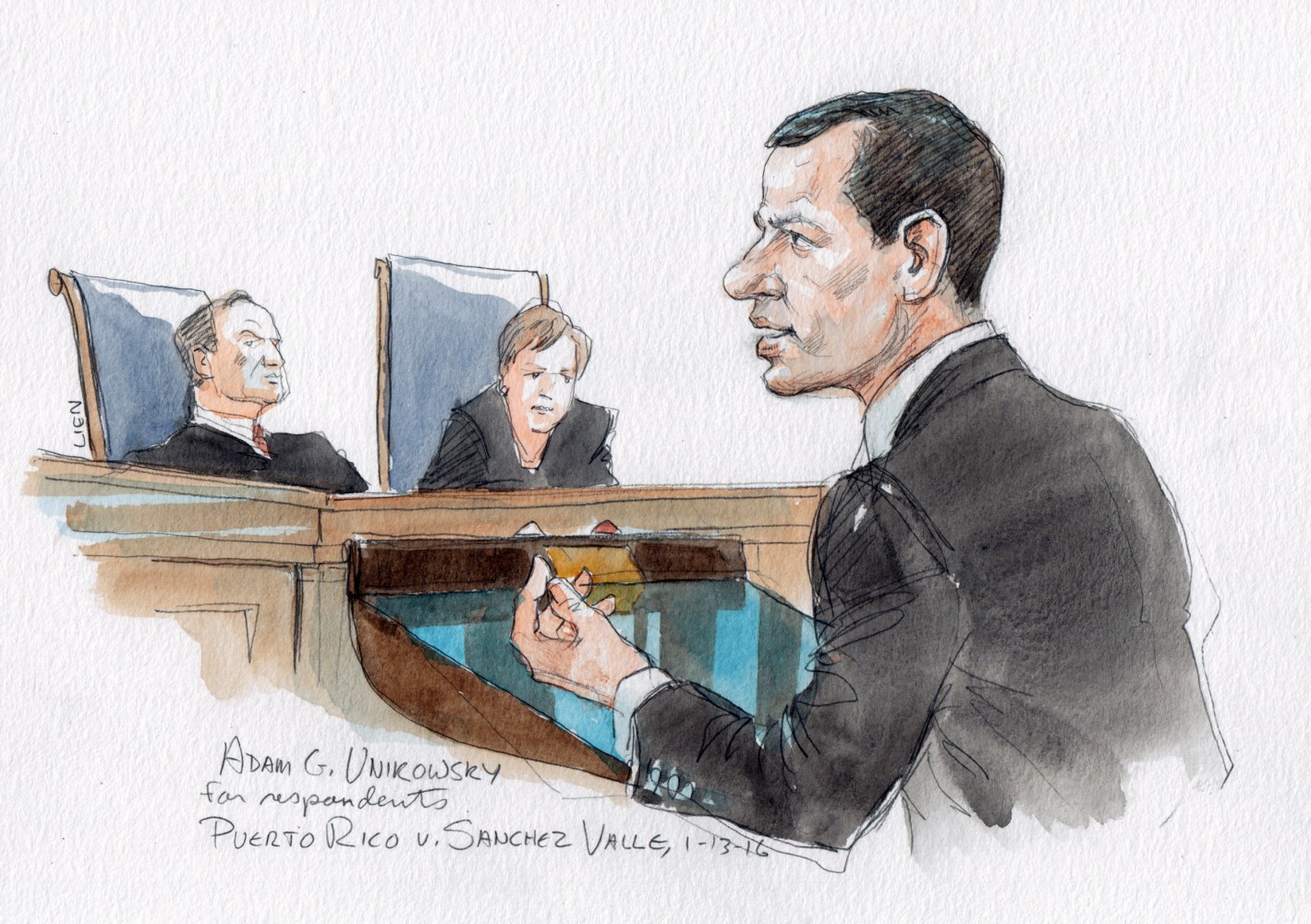

Arguing for Valle and Vazquez, lawyer Adam Unikowski said the issue is simple: "States are sovereign, territories are not."

Adam G. Unikowsky for respondents.Art Lien

Some justices appeared to search for a middle ground. Justice Stephen Breyer said an opinion saying Puerto Rico is sovereign would have "enormous implications." But he suggested the court could find that the island has some aspects of sovereignty that would apply more narrowly to double jeopardy.

"There are different kinds of territories," Breyer said.

The Obama administration has angered Puerto Rican officials by insisting that the island remains a territory subject to the control of Congress.

Justice Department lawyer Nicole Saharsky told the justices that Congress has allowed "increasing self-government" in Puerto Rico and there is no reason to think lawmakers change that. But she said Congress could revise the arrangement because the island remains a territory.

"Congress is the one who makes the rules," Saharsky said.

It’s a form of modern-day slavery and one of the fastest growing crimes worldwide.

Federal and state authorities are stepping up their efforts to fight human trafficking of all types, whether it's minors forced into the sex trade or workers coerced into unpaid labor.

Florida is an epicenter for trafficking.

As the nation marks Human Trafficking Awareness Month, we speak with Amanda Rolfe, President, and Prudence Williams, Executive Director, of the Exchange Club Family Center of Northeast Florida about what’s being done here on the First Coast to raise awareness and bring traffickers to justice.

A fiscal nightmare is brewing in the U.S. territory of Puerto Rico, where employees take home a smaller share of income than anywhere else in the United States.

Some policymakers argue that one of the reasons for this is the Jones Act. That longstanding maritime law requires that shipping between U.S. ports can be done only by American-built and American-crewed vessels.

The Jones Act has come under fresh scrutiny in the wake of the El Faro shipping disaster, which ended in the loss of 33 crew members out of Jacksonville during Hurricane Joaquin.

Author Nelson Denise explores the Jones Act's effects on Puerto Rico and the history of U.S. intervention into that territory's politics in his new book, "War Against All Puerto Ricans." He joins us with more.

And we preview Players by the Sea's production of "Cotton Alley" with playwright Olivia Gowan.

Watchdog Group Questions Ties of Top Puerto Rico Adviser Former New York Lt. Gov. Richard Ravitch has been a leading voice in advocating that the Puerto Rican government be allowed to restructure and avoid payment on its massive debts to creditors. His expertise on distressed debt dates back to the New York City financial crisis of the 1970s, and his current calls for restructuring have gained much attention in Washington.

And throughout the debate on Puerto Rican debt, Ravitch has professed that he has no conflicts of interest, presumably in an effort to be seen as dispensing his wisdom from a kind of financial Mount Olympus. “I represent none in this matter. I am not compensated for the time I have spent in the last year examining the fiscal situation in Puerto Rico,” Ravitch told the Senate Judiciary Committee in a December 1, 2015 hearing.

But now a prominent watchdog group in Washington is sharply questioning Mr. Ravitch’s claims of objectivity and independence, sending a letter to the Senate Judiciary Committee about the potential interests that he may have on the island, even as he advises the government on a financial matter that is reverberating from San Juan to Washington to Wall Street.

In a letter to the committee’s chairman, Senator Charles E. Grassley, Ken Boehm, the chairman of the National Legal and Policy Center, suggests that Ravitch’s extensive work on behalf of the island – he is providing counsel pro bono — may be explained by deeper financial ties or associations. In his letter, Mr. Boehm pointedly questioned Mr. Ravitch’s claim of independence during the Judiciary Committee hearing.

“While that statement may be technically true, it sidesteps a host of relationships of Mr. Ravitch which appear to undercut the claim of independence,” Mr. Boehm wrote.

Boehm then goes on to point out that Ravitch sits on the board of directors for Build America Mutual Assurance Company. BAM is owned by White Mountain Insurance Group, and it has other significant financial arrangements with White Mountain subsidiaries. While BAM has no direct exposure to Puerto Rican debt, its parent and sister companies do.

Boehm adds in his letter to Senate Judiciary Committee Chairman Chuck Grassley: “The resolution of the Puerto Rican debt crisis will have a major impact on at least two of BAM’s competitors for municipal bond insurance business. By any reasonable yardstick, that outcome therefore should affect BAM’s business in a significant way.”

Ravitch did not respond to a request for comment from InsideSources.

A spokesman for BAM declined to offer comment.

Ravitch has been a pro bono consultant to Gov. García Padilla’s administration, according to an article from Vice News. But he has sought to stress his independence, recently telling The Bond Buyer that he is not representing any interest in the Puerto Rico debate.

Puerto Rico officials are scheduling meetings with creditors as soon as Wednesday to begin talks on restructuring its $70 billion of debt, according to two people with knowledge of the matter.

The U.S. territory expects to host at least two meetings in the New York offices of its law firm Cleary Gottlieb Steen & Hamilton LLP over the next two weeks to present the proposal to restructuring advisers representing its creditors, said the people, who asked not be identified because the information isn’t public. Representatives of at least five investor groups have been coordinating with Puerto Rico’s consultants to organize the meetings, the people said.

The creditors themselves, who own securities such as general-obligation bonds and Government Development Bank notes, will have to sign non-disclosure agreements before they can see the proposal, the people said. Lenders typically wait until their restructuring consultant advises them to sign a confidentiality pact before entering debt talks.

Barbara Morgan, a spokeswoman for the development bank at SKDKnickerbocker in New York, declined to comment.

Under Pressure

Puerto Rico is under pressure to persuade lenders to agree to a restructuring accord before July 1, when it must make a $2 billion payment. A commonwealth agency failed to pay $35.9 million it owed Jan. 4 after the administration used revenues pledged to certain types of bonds to meet other obligations. That prompted bond insurers Ambac Financial Group Inc. and Assured Guaranty Ltd. to file alawsuitseeking to prevent the island from diverting revenue in what’s known as a clawback.

The island’s 8 percent general obligation bond due July 2035 rose 0.1 cent to an average of 72.4 cents on the dollar Tuesday, according to data compiled by Bloomberg. A smaller 5 percent general obligation due July 2041 climbed 0.4 cent to an average of 61.4 cents, the data show.

Talks between Puerto Rico and one of its major creditor groups broke down in October after the two sidesfailed to agreeon how to restructure the commonwealth’s debt and inject new capital. The island’s government released arestructuring planin September.

Puerto Rico has been fighting to gain Congressional approval for a change in the law that would enable some of its agencies to file for bankruptcy protection, a process that would allow it to force losses on creditors. It reached an agreement last month with creditors of the island’s main electricity provider, the Puerto Rico Electric Power Authority. Under the terms of the deal, which requires legislative approval, creditors would accept a 15 percent loss on their bonds through a debt exchange.

Add to my calendar

Add to my calendar![[close]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vSAucK_Ug1A-NJ23oS0_Dmkm3JIz_S-XHM0cDVR4JLYercni-6dNK8w_8nmQfZxTixTgJ835yAc4FJ-PbIcdS29pX02RNXgE6AX7Cz6sRId3VJ8SVefXw6b7k=s0-d)