OLDWICK, N.J., Oct 30, 2015 (BUSINESS WIRE) -- A.M. Best has revised the outlook to negative from stable and affirmed the financial strength rating (FSR) of A- (Excellent) and the issuer credit rating (ICR) of “a-” of Cooperativa de Seguros Multiples de Puerto Rico (CSM) (San Juan, PR). Concurrently, A.M. Best has revised the outlook to negative from stable and affirmed the FSR of A- (Excellent) and the ICR of “a-” of CSM ‘s separately rated subsidiary, Real Legacy Assurance Company, Inc. (Real Legacy) (Guaynabo, PR).

The ratings reflect CSM's strong risk-adjusted capitalization, significance market presence within Puerto Rico and its improving, albeit slight, underwriting performance in recent years. The negative outlook is driven by a significant decline in CSM’s policyholder surplus over the past five years along with a weak underwriting performance primarily due to adverse loss reserve development (sinkhole losses in Florida and fidelity losses) and an elevated underwriting expense structure.

The ratings for Real Legacy reflect its strong risk-adjusted capitalization, profitable operating performance driven by solid investment income and somewhat variable underwriting performance.

Partially offsetting these positive rating factors is Real Legacy's geographic risk concentration as a property writer in Puerto Rico and the U.S. Virgin Islands (USVI), which exposes results to the potential for frequent and severe weather-related events, as well as economic, judicial and regulatory changes within its operating environment. Other offsetting factors include the impact of the competitive local marketplace in which the company operates, as well as the elevated underwriting expense ratio. Although the company derives benefits from its affiliation with CSM, one of the leading multi-line insurance providers in Puerto Rico, it also creates the potential for capital or operational pressures, hence the reason for the negative outlook.

Negative rating actions for CSM could result in the near term if operating performance continues to weaken due to deterioration in underwriting performance, a material increase in catastrophe losses beyond expectations that weakens overall capitalization or a continuation of the declining capital position evident over the past several years.

This press release relates to rating(s) that have been published on A.M. Best's website.For all rating information relating to the release and pertinent disclosures, including details of the office responsible for issuing each of the individual ratings referenced in this release, please visit A.M. Best’s Ratings& Criteria Center.

Puerto Rico’s main electric utility gained a few more days from bondholders to negotiate how to restructure $8.3 billion of debt.

Investors holding about 35 percent of the Puerto Rico Electric Power Authority’s debt decided to delay until Nov. 3 the expiration of a forbearance agreement that was set to end Friday, the agency said in a statement. The contract keeps debt restructuring talks out of court. This is the 12th extension since the parties first signed the accord in August 2014.

The extension comes as bondholders and fuel lenders may sign next week an agreement with Prepa, as the agency is known, after reaching a tentative plan in September, Jose Echevarria, a spokesman in San Juan for the utility, said earlier Friday. That potential plan involves investors taking a 15 percent loss in a debt exchange.

Prepa is negotiating with insurance companies that guarantee repayment of about $2.5 billion of debt if the utility defaults. The insurers are considering including in the debt exchange an instrument that would provide liquidity, according to a person familiar with the discussions who asked for anonymity because the talks are private. It’s unclear whether the Prepa can execute a plan to reduce its debts if the insurers don’t back it.

The Financial Industry Regulatory Authority (FINRA) has ordered more fines be paid out linked to the sale of Puerto Rico bonds. The fines were handed out after allegations were made that certain financial institutions failed to properly supervise employees trading bonds in Puerto Rico and allegedly downplayed the risks associated with the bonds. Additionally, FINRA has handed out other fines linked to stockbroker fraud in its stockbroker arbitration hearings.

According to The Wall Street Journal (10/13/15), FINRA fined a unit of Spain’s Banco Santander $2 million for its actions in the sale of Puerto Rican municipal bonds, including failing to supervise employee trading. Santander has also agreed to pay around $4.3 million in restitution to customers who lost money as a result of Santander’s lack of oversight. In agreeing to the settlement, Santander did not admit to wrongdoing in its actions.

Santander is not the first financial institution to pay settlements linked to Puerto Rico bond funds. In September, the U.S. Securities and Exchange Commission (SEC) announced it and FINRA had reached an agreement with UBS Financial Services Incorporated of Puerto Rico (UBSPR) to pay $34 million for failing to supervise a broker whose customers invested in UBSPR-affiliated mutual funds while using money that was borrowed from a UBSPR-affiliated bank. As a result, UBSPR will pay $34 million to U.S. regulators and restitution to clients affected by the Puerto Rico bond funds.

Among the allegations against the UBS former broker are that he downplayed the risks associated with the closed-end funds and misled customers about the risks of investing in funds using borrowed money. The SEC alleged UBSPR failed to have proper procedures in place to prevent or detect the broker’s misconduct.

In June, FINRA ordered UBS to pay $1 million to a Puerto Rican retiree, who alleged UBS brokers recommended the closed-end funds even though they were unsuitable for the investor. The investor, Juan Burgos Rosado, alleged that when he expressed concern about his losses he was encouraged to hold on to the bonds, but ultimately wound up with around $735,000 in losses from his $1 million investment.

Investors who believe they have been misled by their brokers may be able to file a FINRA arbitration against the broker to recover money lost as a result of the broker’s actions. Among unethical actions for a stockbroker are recommending unsuitable investments, churning an account to increase commissions or misleading the investor about the risks associated with an investment.

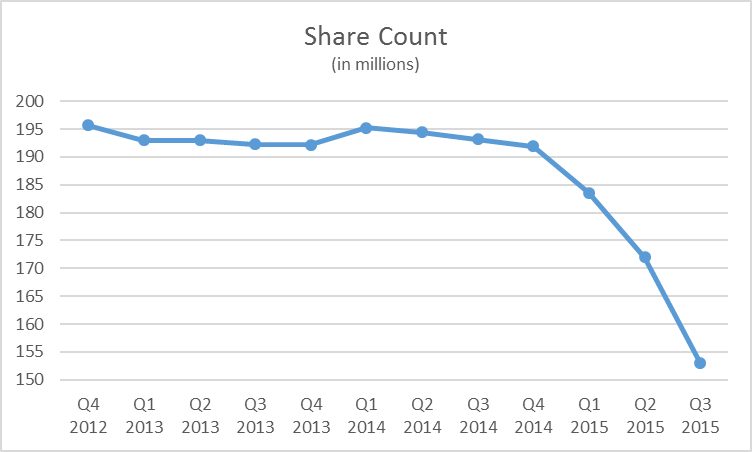

MBIA announced it has repurchased $297M in stock YTD and has authorized another $100M in buybacks.

The company is taking advantage of its depressed share price caused by worries over Puerto Rico to return capital to shareholders in a very accretive manner.

Patient investors will reap rewards as shares trade at only 29% of book value today, down from 75% a mere 21 months ago.

On Wednesday, MBIA, Inc. (NYSE:MBI) announced it had exhausted its previous share repurchase authorization and has approved a new $100M repurchase program. Year to date, the company has reduced the share count by a whopping 20 percent, with a significant acceleration of repurchases in Q3.

Puerto Rico Government Development Bank’s disclosure of its available cash is leaving investors wondering if they’ll be paid on Dec. 1.

The bank, which oversees the island’s borrowings, had $875 million of net liquidity as of Sept. 30, according to a posting Wednesday on the agency’s website. That’s more than twice the $354 million of principal and interest due in 33 days, with $276 million of the bonds guaranteed by the commonwealth. A spokesman for Puerto Rico’s governor reiterated Thursday that while the government plans to make its general-obligation bond payments, it may run out of cash in November and the administration will focus on providing essential services over paying creditors.

“I don’t trust anything they send out,” said Daniel Solender, who oversees about $17 billion as head of municipal debt at Lord Abbett & Co. in Jersey City, New Jersey, and holds the commonwealth’s debt. “It’s just hard to tell what’s real or not anymore. It’s almost more political than anything as to what they decide to do with the next payments.”

Governor Alejandro Garcia Padilla’s administration is seeking to reduce the island’s $73 billion debt load by asking investors to take a loss and delaying principal payments. Officials and commonwealth consultants met Tuesday with bondholder advisers that have signed non-disclosure agreements to discuss a potential debt restructuring after talks with GDB bondholdersfell throughthe week before.

Available Funds

“Certainly it’s a possibility that the government will run out of money, and we’ve said that several times, but we’re trying to make sure that does not happen,” Jesus Manuel Ortiz, the governor’s spokesman, said in San Juan. “If we arrive at that moment, we will have to choose whether to pay the creditors or to continue providing essential services. The governor has always been consistent in his position that we will continue to provide government services.”

The GDB serves as a measure of Puerto Rico’s available funds. The Sept. 30 net liquidity level was the first monthly disclosure of the GDB’s available cash since June, when it gave the May 31 net liquidity amount of $778 million.

“We’re working in two ways,” Manuel Ortiz said during a press conference at the governor’s residence. “As much as in the negotiations with creditors, as in finding measures that will help us maintain the liquidity as quickly as possible to avoid a closing.”

If the GDB and Puerto Rico were to not repay the commonwealth-backed securities maturing Dec. 1, it would be the first default on the island’s direct debt. A Puerto Rico agency in August failed to repay principal and interest on bonds backed by legislative appropriation.

Obama Proposal

Prices on commonwealth bonds differ, depending on whether they are insured against default. The commonwealth-backed GDB bonds maturing Dec. 1 are insured by National Public Finance Guarantee. The securities last traded Tuesday at an average price of 99.8 cents on the dollar, for an average yield of 6.9 percent, according to data compiled by Bloomberg.

GDB bonds without Puerto Rico’s repayment pledge or bond insurance and maturing Dec. 1 last traded Tuesday at an average price of 47 cents on the dollar, Bloomberg data show.

The governor and Antonio Weiss, counselor to U.S. Treasury Secretary Jacob J. Lew, last week at a Senate committee hearing urged Congress to assist the island in its financial crisis. The Obama administration wants Congress to give Puerto Rico broad bankruptcy powers, increase health-care funding, and create a federal fiscal control board that would weigh in on the commonwealth’s spending.

Lord Abbett held, as of Aug. 31, the GDB bonds maturing Dec. 1, including securities guaranteed by the commonwealth and insured by National Public Finance Guarantee and also GDB bonds without Puerto Rico’s repayment pledge, according to data compiled by Bloomberg. Lord Abbett hasn’t participated in talks with the GDB because the firm declined to sign non-disclosure agreements and restrict itself in trading the securities, Solender said. He has yet to hear from the commonwealth or the bond trustee regarding the Dec. 1 payment.

“It just seems like all they’re doing is trying to build their case for Washington and it seems like the odds are pretty low,” Solender said. “And they’re waiting until the last possible minute to take any action.”

To understand how Puerto Rico dug itself $73 billion in the hole, consider the highly attractive tax status of its bonds, which are exempt from local, state and federal taxes everywhere in the U.S. That exemption was granted by Congress in 1917 to help Puerto Rico develop. But without the financial controls Congress also imposed, which have long since been lifted, it's a standing invitation to fiscal misadventure.

Fast-forward a century and Puerto Rico's debt outstrips its gross domestic product; according to Moody's, the island's debt per capita of $15,637 is more than 10 times higher than the average per-capita debt of the 50 states. Debt payments eat up more than one-third of Puerto Rico's tax revenues, starving essential government services and preempting badly needed investments in infrastructure and improvements.

What led to Puerto Rico's economic meltdown is a matter of endless finger-pointing. But whoever lit the match, Puerto Rico's triple-tax exempt bonds fueled the fire. Their tax-free status -- which the bonds of Guam and the U.S. Virgin Islands also enjoy -- made Puerto Rican paper an attractive proposition for investors; even now, more than 50 percent of all open-end municipal bond funds hold Puerto Rico's bonds. Such bonds have also been a bonanza for financial firms: Banks handling Puerto Rico's debt have earned more than $900 million in fees since 2000.

For Puerto Rico's government, meanwhile, bonds came to look like hot credit cards -- max out one, pay it down with another. As the island's economic and fiscal conditions deteriorated, it tapped ever-more creative revenue streams, rolling over debt and papering over deficits with money from bonds secured by future tax revenues.

That was not what Congress had in mind when it granted the triple-tax exemption in the Jones-Shafroth Act of 1917, which set up a new civil administration and granted Puerto Ricans U.S. citizenship.

True, even those who were opposed to making Puerto Ricans into Americans recognized the island needed financial help. As Mississippi's white supremacist Senator James K. Vardaman (whose U.S. Army service included a stint in Puerto Rico) put it, "Those people there are undeveloped, and it is for the purpose of enabling them to develop their country to make the securities attractive by extending that exemption."

Yet Congress also limited public indebtedness to 7 percent (later raised to 10 percent) of the total tax valuation of the island's property. Moreover, the act imposed governing rules that further limited the possibility of fiscal misbehavior. Puerto Rico's governor was appointed by the U.S. president, and had the equivalent of a line-item veto on the budget prepared by Puerto Rico's elected legislature. If the legislature overrode his veto, he had the option of kicking the matter upstairs to the president, whose veto was subject to no such restrictions. Meanwhile, the president also appointed an auditor, operating under the governor, who had oversight of the territory's accounts.

Such paternalistic controls, along with many others imposed on Puerto Rico, understandably came to be seen as insufferable. (Congress even resisted islanders' efforts to change its name from the anglicized "Porto Rico.") In 1947, Puerto Ricans were given the right to elect their own governors, and three years later, a referendum on drafting their own constitution, which they and Congress approved in 1952. In 1961, Congress allowed the then-burgeoning commonwealth to lift the 10 percent limit on indebtedness and set its own. Its constitution was duly amended to create a debt ceiling that is supposedly reached once principal and interest payments hit 15 percent of the average of the past two years' tax revenues.

But that limit was quickly blurred by fuzzy math and executive and legislative legerdemain. So, for that matter, were the commonwealth's subsequent pretensions to a balanced budget. As the National Puerto Rican Chamber of Commerce noted in 2015, total national debt doubled in the 1980s and 1990s, and has tripled since 2000.

Any resident of Detroit could tell you that Puerto Rico isn't uniquely profligate or irresponsible. On the other hand, U.S. territories operate under a curious burden, straitjacketed by federal regulations and laws that hurt their competitiveness, dependent on huge federal transfers, yet lacking meaningful political representation.

Puerto Rico, Guam, and the U.S. Virgin Islands face similar challenges in developing their economies, and each has a history of structural budget deficits and using bonds to cover the difference. Including pension obligations, the U.S. Virgin Islands actually has by some reckonings a higher per-capita debt than Puerto Rico; if Guam didn't have a slightly more restrictive cap on debt (not to mention big economic benefits from the island's military bases), it might well be in the same boat.

The political and economic relationship between U.S. territories and their neglectful overlords in Washington is a blueprint for continuing moral hazard. Under those circumstances, the ability to issue triple-tax exempt bonds seems like an unhelpful anachronism -- another tax gimmick that encourages bad policy choices and increases territorial dependence.

Puerto Rico was granted its triple exemption when it was operating under the equivalent of a federal control board--a condition to which few Puerto Ricans want to return. But given the commonwealth's demonstrated failure to adhere to its own self-imposed debt limits, for the short term at least, greater external controls on its ability to issue debt may be the price it must pay to continue enjoying its tax-exempt funding privileges.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

After years of irresponsible fiscal management, Puerto Rico has few good options to address its growing debt crisis. But in most tales of bad behavior, there comes a point where continued punishment for past mistakes becomes counterproductive. We're reaching that point on Puerto Rico, and the Barack Obama administration has put forward a sensible new approach.

(Citigroup, my employer, has various business relationships with Puerto Rico, including serving as underwriter and market maker in various securities. I've had no involvement in those activities, and this column represents my personal views, not those of Citi.)

Puerto Rico's population and its economy are about 10 percent smaller than they were a decade ago. The poverty rate is 45 percent, only about 40 percent of adults are in the labor force, and unemployment is more than 11 percent.

Given these dire economic indicators, it's not surprising that Puerto Rico has a serious debt problem. At this point, the territory's total liabilities amount to more than 160 percent of the economy, and debt service is projected to be more than a third of government revenue. Over the next five years, the fiscal deficit looks to be $28 billion, and although the Puerto Rican government has proposed aggressive policy actions, these could, at best, only cut the deficit in half. Because the territory's fiscal dynamic is unsustainable, its uninsured debt is selling at discounts of 30 to 70 percent.

Something has to give. Which brings us to the White House's plan.

The first imperative is to restore economic growth. For this, there are no magic bullets, but one useful strategy is to extend the Earned Income Tax Credit to Puerto Rico. The EITC is one of the most powerful, market-friendly mechanisms for encouraging labor force participation, and its absence in Puerto Rico makes no sense.

The Obama administration also proposes removing an anomaly in the Medicaid system. If Medicaid treated Puerto Rico in the same way as it does the 50 states, the federal government would pay for an estimated 83 percent of its Medicaid costs. But because Medicaid payments to the territory are capped, the federal government has generally paid only 15 to 20 percent. In addition, temporary Medicaid payments enacted as part of the Affordable Care Act are almost exhausted, posing a near-term threat to Puerto Rico's Medicaid program.

Establishing an EITC in Puerto Rico and adjusting the share of Medicaid payments paid by the federal government make sense from a fairness perspective. The EITC piece would encourage work, and the Medicaid component would attenuate fiscal pressure on the island. These steps would, though, come at a cost to the federal budget, probably in the billions of dollars per year. The administration should clarify both the amounts involved and how they would be financed.

The island's fiscal governance also needs to be strengthened. Its accounting systems have been shoddy, and revenue estimates have been overly rosy. A period of external oversight is appropriate, to improve transparency and budgetary rigor.

Finally, there's the hard question of what to do about the existing overhang of debt. Write-offs are inevitable; the only question is how to do them in a structured and timely way. We have bankruptcy laws precisely to handle this sort of situation, which would otherwise involve overlapping negotiations with multiple creditors (Puerto Rico has 18 different debt issuers and 20 creditor committees) and probably extended lawsuits.

At the very least, Congress should extend Chapter 9 bankruptcy laws to Puerto Rico's cities and public corporations. Municipalities in the states enjoy this protection, and there's no reason to treat cities in Puerto Rico differently than those in Florida or Texas. This step would cover about a third of the territory's debt.

The more controversial question, though, is whether Puerto Rico's government should also have access to bankruptcy protection. State governments do not, but the administration proposes that territories such as Puerto Rico should.

Bankruptcy would not necessarily mean that less debt would be repaid. So it is not clear that the traditional argument against bankruptcy protection -- that it would raise future borrowing costs -- carries much force. Negotiated write-offs and default would have largely the same effect, but would probably take longer and be messier. Among the options left, the administration's is the least bad.

The plan requires legislation, and in today's polarized Congress, that's a daunting prospect. But as former Treasury Secretary Tim Geithner once emphasized, in a crisis, "plan beats no plan." The administration has one. Its congressional opponents don't.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Puerto Rico's government needs to focus on reform, not on convincing Congress that it should have access to bankruptcy protection to discharge the island's debts.

Members of Congress like Senators Orrin Hatch and Chuck Grassley have expressed doubts over bankruptcy's efficacy. There's a good reason to be skeptical.

Chapter 9 bankruptcy isn't the panacea its supporters would like us all to believe. It's not fairer. It's not more orderly. It's not going to protect taxpayers on the mainland or on the island. And it's definitely not going help the island correct years of government mismanagement.

Getty Images

The Puerto Rican Capitol in San Juan

Proponents of Chapter 9 would have us believe that without it, chaos will rule. It won't. A well-defined process to address an entity's inability to pay already exists under contract law. In fact, Chapter 9 is more likely to produce chaos than prevent it.

Chapter 9 would take months, spur numerous lawsuits and cost hundreds of millions of dollars, given the island's complex debt structures. It would further erode investor confidence in Puerto Rico, exactly the opposite of what we need to begin improving the local economy and to reverse the severe migration trend. It also would force individual investors in Puerto Rico and the mainland to pay for the government's fiscal mismanagement without requiring immediate and credible reforms.

Making matters worse, there is no history for Chapter 9 cases this big. Puerto Rican bankruptcy judges don't have significant experience with Chapter 9, and there is not much precedent upon which they can rely. As a result, as we've seen in several U.S. municipalities, the proceedings are typically arbitrary and can become very politicized.

The only thing Chapter 9 would do is allow Puerto Rico's leaders to kick the can yet again, avoiding the policy and structural changes needed to improve and sustain long-term growth. With Chapter 9, we won't see substantive reforms from the Commonwealth government, and Puerto Rico's residents will be worse off.

If the Puerto Rican government were serious about improving the island's financial situation, there are a number of steps it could take today that would begin to address the island's liquidity constraints and send a positive signal to creditors and the federal government.

For example, Puerto Rico's leaders could privatize, through existing laws, certain public corporations that would otherwise be private on the mainland. It could use public-private partnerships (P3s) to build upon successful P3s implemented between 2010-2012. This would eliminate debt, pension liabilities and shift government expenditures to efficient private sector operators. Additionally, the government could implement procurement reform legislation that has been in place since 2011, saving hundreds of millions through necessary efficiencies. It also could change its very slow and bureaucratic permitting process via executive order, a step that would credibly and quickly reduce costs and encourage investment and growth.

At a recent Senate Finance Committee hearing, Senator Hatch told Puerto Rico that senators need "really well-audited figures" in order to better help the island.

Many people on the island share a concern over the Puerto Rican government's lack of transparency and credibility. The last two fiscal years closed without audited financial statements, which are required by law. In both years, the island's government saw operational deficits after claiming there would be none. During the same two-year period, it missed important revenue targets. Meanwhile, the government increased procurement spending dramatically.

Under these circumstances, how can anyone – local government officials included – know whether there actually is an inability to pay back the island's debt? More importantly, how can anyone responsibly assert that such inability exists, yet not be willing to defend it publicly with financial data?

It makes no sense to retroactively provide access to bankruptcy when the island's leaders have not demonstrated an interest in governing responsibly or dealing with creditors transparently.

For Puerto Rico to seriously request support from the federal government, it must first act seriously. Puerto Rico's leaders can take steps today that require no legislation, no restructuring and no Chapter 9. These steps only require implementation and execution. This is often referred to as "walking the talk." It is time to do more walking and less talking.

Commentary by Jorge San Miguel, a capital member of the law firm Ferraiuoli LLC in San Juan, Puerto Rico. He is also chair of the firm's energy and environmental law practice groups.

Publicly available research shows that the over the last 45 days there have been 23,931 Puerto Rico bond purchases and 33,816 sales.

About 70% of public municipal bond funds held some level of Puerto Rico bonds as of Feb. 2014.

Puerto Rico issues hundreds of different types of bonds. They have varying degrees of credit quality and risks. Many have become mispriced because of the company they keep.

Some short-dated university bonds are showing a yield to worst (the lowest an investor expect) of 100% while trading for 49 cents on the dollar.

There are plenty of Puerto Rico bonds backed by sales-tax listed below trading as much as 40% below real value.

Is Puerto Rico America's Greece?

This article shows how to easily research and identify potential investment opportunities amidst the rubble of the $72 billion Puerto Rico municipal bond marketplace. Make no mistake there is plenty of risk in the Puerto Rico bond market. So buyer beware. But in October 2015 there was news of a potential game changing white knight in the form of the U.S. Treasury Department, which was said to be floating the idea of issuing a "Super bond" to help restructure the commonwealth's debts. There are two views of Super bond proposal:

In addition to urging Congress to offer Puerto Rico the new type of bankruptcy protection, the administration is also recommending that Congress broaden access to the island's Medicaid program, a move that would pump money into its teetering health-care system.

Warren said Treasury officials should do all they can as quickly as they can to help Puerto Rico - much like they did to help the financial system during the 2008 Great Recession. "In my view, the people in Puerto Rico should not be forced to suffer even more so that a handful of wealthy investors can make a 100 percent return on their investments".

Puerto Rico's fiscal problems could turn into a humanitarian crisis, a top U.S. Treasury official warned on Thursday.

Puerto Rico has been trying to persuade different investor groups to sign on to deals to restructure debt.

Yet without bipartisan support in Congress, Treasury is limited in what it can achieve.

"Wall Street should not be believing you can get blood from stone", said Sanders, who rattled off statistics such as the loss of 20 percent of Puerto Rico's jobs since 2006 and a childhood poverty rate of 56 percent.

While Treasury has also called on Puerto Rico to fix its traditionally opaque financial reporting practices and instill more credible fiscal oversight, the proposal is generally in line with what the island itself has said it needs from Congress and its creditors.

Sen. Lisa Murkowski (R-Alaska), the committee's chairman, said that she was sympathetic to Puerto Rico's plight but she needed verifiable numbers about the island's finances before she could help craft a solution.

Like USA states, Puerto Rico is not allowed under current law to seek bankruptcy protection. But on Thursday, skeptical lawmakers told Puerto Rican officials and a high-ranking Treasury aide that such a haircut is easier said than done, and accused the White House of abdicating its responsibility to help Puerto Rico.

"Super Chapter 9 would be de facto amendment of the Puerto Rican Constitution by Congressional legislative fiat without the participation of the Puerto Rican people".

Daniel Hanson, analyst at Height Securities, estimated that the total cost of the Treasury plan is likely about $5.1 billion per year, or $51 billion over 10 years.

Why must one USA territory be required to abide by maritime shipping laws and not another?

A few members of Congress, including New York Senator Chuck Schumer, have advocated in favor of giving Puerto Rico the same bankruptcy rights as USA states.

ALLEN: Puerto Rico's governor, Alejandro Garcia Padilla, is endorsing the White House proposal.

It includes Medicaid expansion and an expansion of low-income tax credits. That puts a heavier burden on the island's budgets during good times, and gives the territory's government nearly no room to maneuver during bad times. Such an offer, or so-called 'superbond, ' could exchange just one credit for various existing bonds, possibly depending on the ranking of those credits, said a source familiar with the situation.

Earlier this week, the Obama administration doubled down on efforts to aid Puerto Rico. The administration proposed to change American law to allow the territory and its municipalities to seek bankruptcy protection. The “Roadmap for Congressional Action” on Puerto Rico seems more calculated to embarrass Republicans than to find an actual solution to the deeply indebted island’s problems. Republicans had serious concerns about previous Puerto Rico bailout proposals. Rather than addressing these concerns, Obama simply cast the issue as a “humanitarian crisis.” The implication? Rejection of his plan would be heartless. But instead of dismissing it, Republicans should demand more substantial concessions on union-friendly federal policies that have helped deep-six Puerto Rico’s economy. Then we’ll see how serious Obama is about this “humanitarian crisis.”

Earlier this year, in a report commissioned by Puerto Rico’s government, three international economists authored a described the territory’s woes. While the report scored the territory for its lack of fiscal controls in the face of a struggling economy, the economists also argued that Puerto Rico suffered because it was forced to adhere to federal laws that have “gnawed at growth.” The “single most telling statistic in Puerto Rico,” they wrote, is that only 40 percent of the working-age population is employed. The biggest obstacle to jobs, the report argued, is that the territory must observe federal minimum-wage law, even though incomes in general are far lower on the island than in U.S. states. A full-time worker in Puerto Rico making minimum wage earns 77 percent of the average wage on the island, compared with just 28 percent in U.S. states. The cost of paying even an unskilled worker is so high that “employers are disinclined to hire.” Even more foolishly, welfare benefits on the island—including food stamps, Medicaid, and subsidies for utility bills—approach mainland levels. Recipients can garner benefits equal to $1,743 a month, more than the average wage on the island. “The result,” the report notes, “is massive underutilization of labor, foregone output, and waning competitiveness.”

Puerto Rico also suffers from the ill-effects of the union-friendly Jones Act—a 1920 law that drives up the cost of goods by forcing ships traveling between U.S. ports to be built and manned by Americans. The restrictions have a particularly devastating effect on the cost of transporting goods to and from U.S. island territories or states, such as Puerto Rico and Hawaii. Neighboring islands that aren’t U.S. territories pay far less. “Exempting Puerto Rico from the U.S. Jones Act could significantly reduce transport costs and open up new sectors for future growth,” the economists’ report argues. Other factors impeding Puerto Rico’s growth include complex local regulations on banking, an inefficient energy sector that drives up the price of power, and difficulties in registering property, obtaining business permits, and paying taxes. As the economists observe, the territory ranks 47th (out of 189 governments) in the World Bank’s ease-of-doing-business index. The United States ranks seventh.

The president’s plan says zero about these issues. Its only mention of welfare benefits is a demand for island residents to get more from Medicaid. Its chief suggestion for stimulating economic growth is to extend the Child Tax Credit and the Earned Income Tax Credit—a tool for rewarding low-income workers who stay employed—to Puerto Rico’s residents.

Republicans should make reform of Puerto Rico’s anti-business climate central to any plan to help it. That would include not only exemptions to U.S. labor laws that don’t make sense in an economy like Puerto Rico’s, but also assurances from the island’s leadership that it will reform its anti-growth regime of bad regulations and wrongheaded laws.

In the past, Republicans in Washington took a dim view of granting bankruptcy for Puerto Rico. But the GOP may be ignoring an opportunity that the Puerto Rico crisis presents for dealing with a problem closer to home: the state and local pension crisis. With his proposal, President Obama was careful to wall off the municipal bankruptcy code from larger changes. He and his political allies, especially public-sector unions, fear that helping Puerto Rico might make it easier for municipalities or other entities within states—including deeply indebted pension systems—to file for bankruptcy protections. In places like Illinois, New Jersey, and California, where taxpayers’ efforts to reform public-sector debt run into one stumbling block after another, bankruptcy might be the only way of clearing away these steep fiscal obligations. The GOP should use Obama’s Puerto Rico gambit, clearly a political ploy, to start a discussion on municipal debt that the administration and its allies would rather not have.

The Obama Administration has proposed a plan to rescue the U.S. Caribbean territory of Puerto Rico from $72 billion in debt.

The Treasury Department unveiled a plan on Wednesday that would allow the island to seek bankruptcy protection in federal court so it can restructure its debt, an option that is only available for individual cities and municipal agencies.

Puerto Rico's Government Development Bank broke off talks with creditors Wednesday when they refused to accept lower payments on existing government bonds.

The Treasury Department also wants to create a financial control board for Puerto Rico, extend the federal income tax credit for the working poor to the island's impoverished residents, and overhaul Puerto Rico's Medicaid program, the joint federal-state health insurance program for poor Americans.

A statement issued by Treasury Secretary Jacob Lew urged Congress to approve the plan, saying it was the only entity "to provide Puerto Rico with the necessary tools to restructure its financial liabilities in a fair and orderly manner." The statement also warned that all the emergency actions the island has taken to address the problem will be exhausted within months.

About 45 percent of Puerto Rico's 3.5 million people live in poverty, which has forced scores of them to flee to the mainland United States. Puerto Ricans are U.S. citizens, but cannot vote in presidential elections. The island has a non-voting member in Congress.

Puerto Rico's debt-laden power utility, PREPA, has extended forbearance agreements with bondholders and lenders that will allow it to keep negotiating a restructuring deal with other creditors, it said on Thursday.

PREPA, facing more than $8 billion in debt, said in a statement that it had extended through Oct. 30 an agreement that was to expire Thursday night, preventing creditors from calling a default and suing the agency as restructuring negotiations go on.

The lenders and bondholders who signed the extension have already agreed to a restructuring deal with PREPA, but the agency needs the support of bond insurers like Assured Guaranty and MBIA's National Public Finance Guarantee for the deal to work.

PREPA said it will use the extra eight-day window to try to nail down terms with the insurers, who are not parties to the forbearance agreement and could potentially sue PREPA or push for a financial receiver.

"We continue to make progress in our comprehensive transformation that shares the burden among key stakeholders," PREPA Chairman Harry Rodriguez said in the statement.

The forbearance agreement was first signed in 2014, when restructuring talks at PREPA got underway.

Sides have extended it many times since. The insurers were initially party to the agreement, but exited earlier this year and have since turned up the heat on PREPA, threatening legal action and resisting concessions even as bondholders and lenders agreed to haircuts.

The deal signed by those creditors would involve a 15 percent reduction in payment in exchange for new, higher-rated debt.

Sources familiar with the negotiations told Reuters this week that PREPA and the insurers are making significant progress, and are confident they will reach a deal.

PREPA is a key piece of Puerto Rico's debt puzzle, and resolving its financial woes could go some way toward helping the island tackle its larger $72 billion debt load.

The Puerto Rico Electric Power Authority and insurance companies that guarantee repayment on some of its bonds are in talks to delay payments to free up cash and and help restructure $8.3 billion of debt, according to two people with knowledge of the matter.

A compromise with MBIA Inc., Assured Guarantee Ltd. and Syncora Guarantee Inc. is the missing piece in a plan announced last month in which some holders of uninsured bonds agreed to take a 15 percent loss in a debt exchange. The parties are working out details that would ease near-term debt payments, said the people, who asked for anonymity because the talks are private.

The negotiations come as Prepa, as the agency is known, won another eight days from investors that hold about 35 percent of its debt, and fuel lenders, to negotiate how to restructure its securities, according to Harry Rodriguez, chairman of Prepa’s board. The forbearance agreement, which now expires Oct. 30 and was set to end Thursday, keeps discussions out of court. This is the 11th extension since the parties first signed the agreement in August 2014. A Prepa restructuring would be the largest ever in the $3.7 trillion municipal-bond market.

Lisa Donahue, Prepa’s chief restructuring officer, said Tuesday at a meeting organized by Puerto Rico’s Chamber of Commerce in San Juan that she’s confident the utility will come to an agreement with its bond insurers.

Jose Echevarria, a spokesman in San Juan for Prepa, declined to comment. Michael Corbally, a spokesman for Syncora, and Ashweeta Durani, spokeswoman for Assured, declined to comment.

Greg Diamond, a spokesman for MBIA, reiterated that the insurer continues to work with Prepa, local government officials and other creditors toward a consensual solution.

Bankruptcy Proposal

The monolines, which insure about $2.5 billion of Prepa debt, are considering embedding in the potential debt exchange an instrument that would provide liquidity, one person said. Prepa and the bond insurers may reach a tentative agreement as soon as Friday, the other person said. The utility faces a $196 million interest payment on Jan. 1.

Questions about the oversight of Puerto Rico’s broader finances is a sticking point in the discussions with the insurers, one person said. Governor Alejandro Garcia Padilla has filed legislation that would create a five-member fiscal oversight board, with those panel members selected by the governor and approved by the Senate. A board on which members are separate from political leadership would provide better transparency and management of the island’s finances, the person said.

Prepa bondholders have objected to an Obama administration proposal released Wednesday that asks Congress to give the commonwealth and its municipalities access to bankruptcy protection to help reduce the island’s $73 billion debt load. The governor announced in June that debt payments were unsustainable.

Puerto Rico is $73 billion in debt, but in a calculated decision, the governor of Puerto Rico and his Commonwealth political party recently caused Puerto Rico to default on one of its debts by not paying a $58 million obligation.

We, the proud residents of Puerto Rico; want to pay every cent that is owed. But the failure by the governor to pay this debt is actually a not-too-subtle attempt to make Puerto Rican statehood less appealing to both Congress and to the people of Puerto Rico.

Millions of Puerto Ricans forcefully object to Governor Garcia Padilla’s use of such Machiavellian’s political tactics. Puerto Ricans are American citizens that strive to have the same standard of living as citizens living in each of the fifty states. We are legally required to follow the laws and the Constitution of the United States, but because we are not a state, we have far fewer tools at our disposal to achieve this.

Many former Puerto Rican governors exceeded Puerto Rico’s approved colonial budgets in their desire to provide our citizens with the same standard of living that our fellow American citizens enjoy in the mainland. Today this failure of leadership, and frankly, irresponsibility, is compounded by the fact that the island is collapsing under the weight of its ancient territorial, political, and economic infrastructure. Since 2004, Puerto Rico has been in the grip of a severe economic, financial, and demographic crisis. This crisis has forced 83,000 Puerto Ricans to migrate to the mainland in the past year alone to look for jobs and better opportunities.

Importantly, the benefits and responsibilities enjoyed by our fellow American citizens are today unattainable for Puerto Rico because we lack full political representation at the federal level. However, a solution exists and it is clearly stated in the 2011 Report by the President’s Task Force On Puerto Rico’s Status: “Resolving the island’s political status is essential to restoring the health of Puerto Rico’s economy and to improving our security”.

In 2012, the government of Puerto Rico held a two-part plebiscite in which 54 percent of the voters rejected continuing under the present territorial status, and in which 61 percent of voters who selected one of the three constitutionally viable non-territorial options voted in favor of statehood. After issues with the plebiscite were raised by the Commonwealth political party that lost the referendum, Congress appropriated $2.5 million for an education campaign in order for the government of Puerto Rico to conduct yet another fair, transparent and inclusive plebiscite. But in the aftermath, Padilla and his Commonwealth party have not taken any significant actions to approve such a bill and conduct a new referendum.

Their inaction promotes the perpetuation of a morally and economically bankrupt colonial status and is against the democratic will of their own constituents – the people of Puerto Rico – who have formally withdrawn their consent to being governed in this way and have expressed a preference for statehood over all other constitutionally-viable options.

There should and must be no abrogation of debts. Puerto Ricans want to pay what is owed, but regrettably, at this moment our island needs federal assistance, expertise and supervision, to enable an orderly debt restructuring mechanism as well as the appointment of a Fiscal Control Board similar to the one Congress appointed for Washington DC in 1994 to oversee and attain this goal. Moreover, we cannot begin Puerto Rico’s road to recovery without initiating at the same time the process of resolving our undignified colonial status, and we are asking Congressional political leaders in Washington DC, to put this issue front and center on their agenda.

All other options are palliative measures until we are given the opportunity to become the fifty-first state of the Union - a status demanded and desired by a majority of our residents. We are American citizens and we do not deserve to be ignored anymore by our local government or the federal government. The leaders of our commonwealth and our nation have the civic and moral obligation to do the right thing for the 3.5 million American citizens living on the island of Puerto Rico.

Saldaña is former president of the University of Puerto Rico.

any Puerto Rican will tell you, these are difficult times for the island and all who love it. Faced with major fiscal and health-care crises, its 3.5 million American citizens have done all they can to provide for their families. But they need help from the U.S. — and it's time to discuss seriously how we plan to provide it.

That's why I attended El Encuentro de la Diaspora, a first-of-its-kind conference in Orlando last week. The conference, which convened elected officials, nonprofit leaders and labor and grass-roots activists, provided a sense of purpose for Puerto Ricans living in the U.S. in the island's time of need. Just as important, it was a show of strength for a sleeping giant in American politics: the Puerto Rico vote.

The island needs an organized legal framework to coordinate its debt payments with its many creditors. Its status as a commonwealth, however, currently excludes it from Chapter 9 bankruptcy protections — just the bulwark it needs against its crushing obligations. I joined other attendees in calling on Congress to extend Puerto Rico these protections so it can manage its debt and get its economy back on track.

I'm also passionate about finding solutions to Puerto Rico's health-care crisis. Sixty percent of Puerto Ricans receive their health care through Medicare, Medicare Advantage or Medicaid. They pay the same taxes as other Americans, but the 2 million Puerto Ricans who depend on these programs for care receive less health-care funding than anyone on the mainland.

Even worse, the federal government has proposed a devastating 11 percent cut to Puerto Rico's Medicare Advantage, scheduled to take place next year. Deep cuts to an already underfunded system are unfair and discriminatory; Puerto Ricans have a right to health care like everyone else who pays into our system. I spoke forcefully at El Encuentro against these cuts, and called on Washington to provide equal health-care funding for families in the commonwealth.

The fiscal and health-care crises facing Puerto Rico, which have already caused suffering for so many, present an unprecedented opportunity for Puerto Ricans in the U.S. to make their voices heard. There are more than 8 million of us — more than 1 million in Florida alone.

By channeling its passion into organization, the Puerto Rican diaspora community made El Encuentro more than just a conference. It was the beginning of a movement that will make us a force to be reckoned with at the ballot box – in 2016 and beyond.

Wait, I can sense your hesitancy. Is it because of the quirkiness of the number? Because I refuse to sit here and listen to any hate speech about “51,” you rabid anti-semiprime-ite!

Or … maybe it’s because you don’t think the Caribbean island’s star will fit in the already over-crowded bluey recess that is Old Glory’s canton. Well, we could always just hide it in one of the stripes. Better yet, just replace South Dakota’s star with it. No one will care. Done and done.

Oh, I see. This is about money. Sure, Puerto Rico’s on the verge of filing for bankruptcy. But is there anything more American than being broke right now?

Because if you’ve been struggling to find just one issue to agree with Jeb Bush on, this is it: He’s 100 percent down with PR statehood.

Still not convinced? Here, a very palindromic 15 ways the Rico-suave US territory should become state No. 51, leaving Guam and American Samoa back at the kiddie table (sorry, guys).

1) The Vandy man can

If it’s good enough for the Vanderbilt family, it’s good enough for us. Back in 1919, Frederick William of said Dutch dynasty built the not-coincidentally named Condado Vanderbilt. It recently reopened after a $200 million reno; if you’ve never used one of their business butlers, you’re truly missing out. From $225.

2) I’m about to go HAM(mam)

Modal TriggerPhoto: Condado VanderbiltSpeaking of the joint, P.S., Puerto Rico’s first and only hammam can be found at The Spa at Condado Vanderbilt.

There’s not one, not two, but five Miss Universe winners from the island (no, thank you, Mr. Future President of the Universe Donald Trump).

5) Now we’re cookin’

Modal TriggerXavier Pacheco — to the right of Navy restaurant’s Camille Becerra — helms La Jaquita Baya.Like any good countrymen, Puerto Ricans like to eat — maybe even more so than Mississippians — so it’s little wonder the island is home to a great many top chefs and their respective kitchens: Juan Jose Cuevas (1919 Restaurant), José Santaella (Santaella), Mario Pagán (Laurel), Pedro Álvarez (AlCor Foods Inc.), Jose Enrique (El Blok), Wilo Benet (Pikayo), Alfredo Ayala (Chayote), Xavier Pacheco (La Jaquita Baya), Kevin Roth (La Estacion), the list goes on.

6) Branching out

Modal TriggerPhoto: Puerto Rico Tourism CompanyWhile it’s probably no picnic for the thirsty trees themselves, there is such a geographical curiosity as a tropical dry forest, so-taxonomied for their unusually long droughts. Outside of Hawaii, Puerto Rico would be the only state to have them. But if you insist on the rainy varietal of trees, verdant and hiker-friendly El Yunque — the only rainforest in the US National Forest System — is always willing to wet your whistle.

7) Blue light special

Modal TriggerPhoto: Puerto Rico Tourism CompanyOutside of a few Berlitz-cribbed foreign words embarrassingly butchered at a waiter, rarely do we vacation with an expanded vocabulary. But Puerto Rico’s got a good one: bioluminescence, a k a “living light.” In bay form, it’s a pool of millions of one-celled dinoflagellates — oh wait, another sexy one! — that glaze the water in neon blue. There’s only seven of these bio bays in the world, and Puerto Rico has three (including the Guinness World Record holder for brightest: Mosquito Bay).

8) ‘A three-hour tour … a three-hour tour’

Puerto Rico is home to a real-life, really named Gilligan’s Island (the western-most cay in Cayos de Caña Gorda), just a quick boat ride away from Copamarina in Guánica; ideal for snorkelers and professors, alike. See it by inflatable beer-friendly Jacuzzi (towed by a real boat) when you stay at nearby Copamarina Beach Resort & Spa in Guánica. From $269 (Ginger and Mary Ann not included.)

9) Get on board

Other than Cali, Hawaii and Florida, Puerto Rico would be one of the few states perfect for surfing year-round. San Juan-based Courtyard Isla Verde‘s gnar surf-n-stay package can get kooks and groms started with daily lessons. From $199.

10) Second to nun

Modal TriggerPhoto: Hotel El ConventoSing it, sister, at Old San Juan’s centrally located, centuries-old Carmelite nunnery, Hotel El Convento — the only Small Luxury Hotels of the Worlder in the ‘hood. Have the property’s chef give you an herb garden tour with bottomless bubbly and then prep your meal. Then lock down the sail-n-stay package to San Juan Bay, from $270/night.

11) Take the money and rum

Modal TriggerPhoto: Bacardi ArchiveLike we need to tell you Puerto Rico is home to both the Bacardi and Don Q rum factories (as you already did your mini-bottle research on the plane coming over). But you might not know the island also has several craft beer brewers like Barlovento Brewing Company in Manati, Boquerón Brewing Company in Cabo Rojo, FOK Brewing Co. in Caguas and Señorial Brewing Co. in Ponce, just to name a few. But back to that rum. Famed Gotham mixologist Lynnette Marrero’s secret rum cocktail, Chino Latino, is made with 2 oz. Don Q Cristal, ¾ lemongrass lime cordial, ½ oz. coconut water and ½ oz. lime juice. You’re welcome.

12) You clammed up

Modal TriggerPhoto: La ConchaYou can chow down inside a giant shell-shaped restaurant, Perla, at San Juan’s La Concha Resort. The menu’s fittingly mostly surf plus a li’l turf.

13) Sugar rays

Hear ye, hear ye — bikini season is dead, long-live fat season! The Doubletree by Hilton San Juan is getting things started with its “Sweet Treats” package, including signature fresh baked chocolate chip and walnut cookies at check-in, handmade gourmet chocolates, comp’d breakfast and, randomly, admittance to the Puerto Rico Museum of Art. From $249.

14) Fiesta, forever

A little bit Mardi Gras — OK a lot bit Mardi Gras — La Placita de Santurce in San Juan transforms from mild-mannered marketplace by day into an orgiastic food-and-cheap booze-fueled dance party by night, especially on weekends (the Puerto Rican word “weekend” means Thursday-Monday).

15) Tax breaks on fleek

Totally unrelated to its current financial whoops-a-daisy, Puerto Rico is gently reminding the world of its three-year-plus-old, tax-haven-y legislation which provides tax breaks for business owners and investors looking to relocate to somewhere sunnier than Wall Street. “Act 20” offers a flat 4 percent tax on earnings, as well as 100 percent tax-exemption on dividends or profit distributions from export services (you must employ at least 3 people). “Act 22” exempts business from taxes on dividends and capital gains, red meat for hedge-funders, asset managers and traders. I don’t understand what I just said, but there, I said it.

The tinted-lensed denizens of Puerto Rico's Guánica municipality are as beautiful as the land itself.

While Europe agonizes over the Greek debt crisis, the United States is saddled with one of its own. Individual investment portfolios are replete with $72 billion in bonds issued by Puerto Rico’s government and its agencies, and since August this US Commonwealth has been in default. While federal law allows municipalities to restructure their debts under Chapter 9 that option is unavailable to states or US territories.

The latest proposal designed to remedy the Puerto Rico debt calamity is a so-called “superbond” plan. The details are still sketching, but one scenario entails swapping existing bonds for new ones managed by the federal Treasury. While the Treasury would not guarantee the debt it would be responsible for managing some of Puerto Rico’s tax revenues, thus decreasing the likelihood of a default on the replacement bonds.

It is unclear, however, whether the old bonds would be exchanged for new ones of equal value. Assuming this scheme can leap over the numerous political and legal hurdles necessary for implementation there remains the question of how much of a dent this could make in $72 billion in unpayable debt. Although a noble effort this strategy amounts to affixing a very small bandage over a rather deep financial wound.

To begin with, how did Puerto Rico get into this mess? Investors bought Puerto Rico’s bonds at a time when its finances, by all appearances, were strong enough to repay its debts. Government budgets ultimately rest atop the employment base sustaining them. While tourism and agriculture employ thousands those sectors are too small to absorb all able-bodied workers. One remedy for the island’s unemployment woes has been fostering other economic sectors, such as manufacturing. Due to the federal minimum wage Puerto Rico’s payroll costs are high compared to its Caribbean neighbors. Federal health and safety regulations also add to the cost of doing business. And under the 1920 Jones Act, goods exchanged between Puerto Rico and the US mainland must be shipped via U.S.-flag carriers – among the most expensive in the world. Thus, it has not been easy to attract manufacturing plants to Puerto Rico.

In a bid to stabilize, if not bolster, Puerto Rico’s economy the federal government provided enterprises operating in Puerto Rico with industrial tax incentives. These enticements, under Section 936 of the Internal Revenue Code, the cornerstone of the island’s manufacturing base, were dismantled with devastating economic consequences. Deemed “corporate welfare” by many, the federal government instated a ten-year phase out for these 936 incentives beginning in 1996. The numbers speak for themselves. The Bureau of Labor statistics reported that in 1995, the year before Section 936 was put on the chopping block, there were 159,000 manufacturing jobs in Puerto Rico. Twenty years later there are fewer than 75,000 employees in this sector — a decrease of more than fifty percent. Fewer manufacturing jobs translates into declining tax revenue for a debt-ridden Puerto Rican government.

The decimation of Puerto Rico’s manufacturing base has yielded other economic consequences. Unable to find work hundreds of thousands of islanders, particularly the young and college educated, have migrated to the US mainland in the past decade. As US citizens there is no legal impediment to their relocation. Whereas New York City was the prime destination for the great migration of the 1940s and 50s today’s preferred terminus is Orlando, Florida. A critical section of the next generation, the very people needed to lead the island out of its economy morass, are departing. The consequences of their departure will be felt for decades to come.

Despite the gravity of this situation there’s been, so far, an eerie silence from Capitol Hill. For the time being Republican lawmakers, consumed by internecine warfare, have shown little interest in touching Puerto Rico’s debt disaster. Individual investors are paying the price as are the tens of thousands of Puerto Ricans who are packing their bags to head stateside. This migration, a rather quiet exodus when compared to its counterpart in Europe, further erodes Puerto Rico’s capacity to put its financial house in order.

The “superbond” idea, a laudable effort, is simply too meagre a remedy to fully tackle this crisis. A more realistic short-term solution is amending federal law to allow the Commonwealth of Puerto Rico to file for Chapter 9. In the long haul the island’s economy cannot recover to the point where it can repay its debts without a restoration of tax incentives that attracted industries there in the first place. Both remedies, sadly, are unlikely in Washington’s current climate. Given the current state of affairs the most likely scenario is a continued decline in Puerto Rico’s economy and Puerto Ricans displacing Cubans as the largest Latino community in the State of Florida.

Amílcar Antonio Barreto is an associate professor of political science, international affairs and public policy at Northeastern University. He is also the director of its MA Program in International Affairs.

As U.S. officials talk about ways to save the debt-trouble territory, it should consider changing laws to allow states and territories to file for Chapter 9.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}