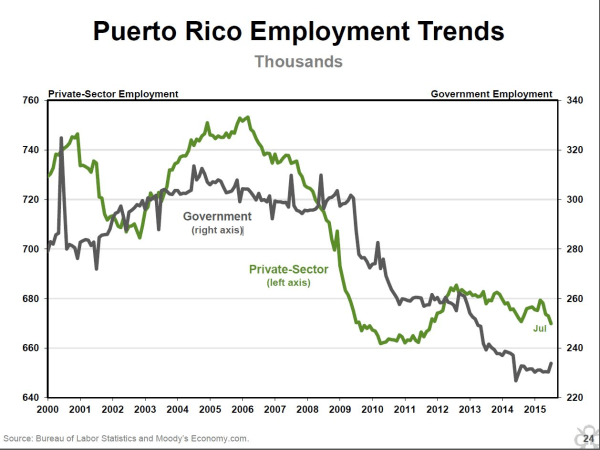

Puerto Rico’s governor extended a Sunday deadline for a group of government officials to deliver a draft of a restructuring plan that is widely anticipated by investors.

The governor’s chief of staff,Victor Suarez Melendez,said in a statement that the deadline has been extended to Sept. 8. He attributed the delay to officials’ preparations for Tropical Storm Erika.

“Since the government’s efforts in the past days have been focused on preparing for the possible impact of Tropical Storm Erika, the work of the designated group, the consultant’s analysis, and the final drafting of the document have not been completed,” Mr. Suarez Melendez said.

Puerto Rico Gov.Alejandro Garcia Padillasaid in June that the island’s debts are unpayable. Investors in the island’s bonds, which are widely held by U.S. mutual funds, say they hope the draft restructuring plan will shed light on how much debt relief the government intends to seek.

By Mike Cherney

Delivery now set for Sept. 8 as officials prepared for Tropical Storm Erika

As Puerto Rico grapples with crippling debt and double-digit unemployment, a far-fetched idea to tackle the US territory’s economic woes may be gaining modest traction – one that would seePuerto Ricobreak off from the United States to re-join Spain.

“By returning to Spain, we’ll have autonomy,” said José Nieves Seise, who in 2013 founded the groupReunification of Puerto Rico with Spain. “With autonomy Puerto Rico could have sufficient powers to boost the economy and attract foreign investment.”

On Sunday, as thecommonwealth’s financial crisiscontinues to cast a shadow over its relationship with the US, some of the group’s more than 3,000 members will gather in Puerto Rico for their annual assembly to explore the idea of becoming the 18th autonomous region of Spain.

The movement is based on a mix of nostalgia and alternative history, with Nieves Seise pointing to what he calls a flawed depiction of Puerto Rico as a colony of Spain. “In reality it was an integral part ofSpain. The US invaded us in 1898, and they separated us against our will.”

The split was superficial, he said, highlighting the similarities that endure between Spain and Puerto Rico to this day. “Puerto Ricans love the Spanish people; we’re Spanish. We want to return to the country to which we belong,” said the 43-year-old.

The idea is a long shot, as it relies on contesting the 1898 Treaty of Paris, which laid out the framework for the island to change from Spanish to American hands. Still, the group met with Spanish officials at the consulate in Puerto Rico last year. “Our goal was just to let them know that our movement exists and that it’s something serious.” This month Nieves Seise plans to send a letter to Spanish King Felipe VI, introducing the monarch to the movement.

Nieves Seise decided to launch the group out of frustration, after repeated calls to address Puerto Rico’s status were ignored by the US. A 2012 referendum found 54% of the island’s 3.5 million inhabitants favoured changing the island’s current territorial status. The financial crisis has also injected renewed vigour into the campaigns pushing forAmerican statehood for Puerto Ricoand those pushing for independence.

Nieves Seise rejected these rival campaigns, denying claims by critics who argue that Puerto Rico had fewer freedoms under Spanish rule. Instead he touted the economic advantages of joining Spain, arguing that benefits such as coming under the EU umbrella would allow Puerto Rico to move forward after nearly a decade of economic stagnation.

The island would also be afforded political rights currently denied to them by the US, he said. “Right now, we can’t vote for the president of the United States, we have limited representation.”

The group has already managed to secure the backing of some in Spain, with a handful of support groups cropping up in recent years in the cities of Málaga and Granada.

In January, about a dozen supporters in the province of Castellón formally launched a group, said Spaniard Cristofer Pons Rodríguez. “Personally, I was attracted to the idea of creating a community of citizens that share the Spanish culture,” said the 24-year-old, drawing parallels with the Commonwealth or Francophonie. “It would be about creating a Hispanic bloc as an alternative to the Anglo-Saxon world, to defend our interests.”

As Spain struggles to shake off the lingering effects of a double-dip recession, Pons Rodríguez dismissed concerns that taking in Puerto Rico and its $72bn worth of public debt could dampen Spain’s tepid economic recovery. “This shouldn’t be an impediment to working together,” he said. “The more united we are, the better chance we have of overcoming issues like debt.”

To date the movement has not received any kind of formal response from Spanish authorities. Recently Puerto Rican Iván Arrache called on Spain to take action. “Are they going to leave us to do all the work ourselves?,” he wrote inEl Diario de La Marina. “It takes two to tango.”

Spain stands to benefit from taking Puerto Rico into its fold, he said. “Don’t they appreciate the impact this would have against Catalan separatism and how this would help foster the idea of a united Spain?”

After two years of nurturing the movement in Puerto Rico, he said, it was time to establish whether there is any official interest in the idea from Spain. “Spain needs to give us a token of good faith, even if it’s just symbolic,” he said. “Many of us here are ready to give our all. All we’re asking for is something from the other side.”

Due to "turmoil in the global markets," Puerto Rico has decidednot to go aheadwith a controversial proposal to borrow $750M for improvements to its water and sewer authority.

The government seemed to have also decided it could not borrow the money at an affordable interest rate. Investors seemed taken aback by the move, which aimed to sell new bonds while telling the U.S. Supreme Court it had to restructure its old debt.

In a Wednesday press briefing, New York Federal Reserve President William Dudleyspokeon various economic issues, including endorsing Congressional action in response to Puerto Rico's financial crisis.

Addressing a question regarding how the Fed can help the situation in Puerto Rico, Dudley suggested that Congress would be more fit to act on the issue.

"The most important thing," Dudley said, "would be [...] if Congress could actually pass legislation granting the authority to do Chapter 9 bankruptcy filings for Puerto Rico, which they do not have today."

Federal Reserve Bank of New York

The New York Fed President continued, "I think that would be helpful, because it could help facilitate an orderly restructuring of their debt which is probably going to turn out to be necessary."

Currently there are two bills, one in the House and one in the Senate, proposing that some of the island's entities - such as its beleaguered public utility - be allowed to restructure its debts under Chapter 9 the way Detroit has done. While states can allow their municipalities to file for Chapter 9, this is not the case with Puerto Rico, which is a U.S. territory.

Dudley also pointed to two white papers written by the Fed,one in 2012and anupdate in 2014, that outlined the issues facing Puerto Rico and options to improve economic performance.

On August 3rd, Puerto Rico defaulted on its full payment of its bonds for the first time in the commonwealth government's history. On top of a deepening economic crisis, Puerto Rico is also experiencing one of the worstdroughtsin the territory's history.

To Guam Governor Eddie Calvo, the only similarity between his Pacific island and Puerto Rico is that they’re both tropical U.S. territories.

The $3.6 trillion municipal-bond market appears to agree.

As Puerto Ricostrugglesto find investors after a fiscal crisis pushed it to default, Guam on Tuesday finished its biggest sale in six years a day ahead of schedule. Officials boosted the deal by $8 million to $413 million as investors lined up to buy securities from the island of 160,000 people, which is prospering from record tourism and an upsurge in private investment since Calvo took office in 2011.

For investors like Nuveen Asset Management and Thornburg Investment Management, which spurned Puerto Rico securities as its finances worsened, Guam offers a less risky way to own bonds with interest that’s tax-exempt nationwide. It shows in Guam’s tax-backed bonds, which priced at a top yield of 4.18 percent, compared with 15 percent on similar Puerto Rico debt.

“There are a lot of encouraging trends in Guam,” said John Miller, co-head of fixed income at Nuveen, which oversees more than $100 billion of munis, including $396 million of Guam bonds. “A lot of state funds in the marketplace have really reduced their Puerto Rico exposure, and if you’re not getting enough state paper, this deal could be a better candidate.”

Sentiment Gulf

The difference in investor sentiment between Guam and Puerto Rico mirrors the 9,372-mile (15,080-kilometer) distance between the two islands, whose bonds are exempt from federal and local income taxes in every state.

Puerto Rico has been downgraded deeper into junk status repeatedly since last year and may reveal a plan as soon as next week to delay payments on some of its $72 billion of debt. Guam has just $2.5 billion of outstanding securities and has a cap on how much it can issue, which it’s close to hitting. That prevents the runaway borrowing to pay bills that’s left Puerto Rico reeling.

The cash-strapped commonwealth has seen its market access dry up. Underwriters had initially planned a bond offering for Puerto Rico’s Aqueduct and Sewer Authority as soon as Aug. 18. It’s now considered day-to-day, meaning the timing is unclear.

Guam will use proceeds from Tuesday’s sale to refinance some higher-cost general-obligation debt it issued in 2007 and 2009, according to offering documents. The new securities, backed by a sales tax levied on businesses, have an A rating from Standard & Poor’s, the sixth highest. That’s above S&P’s BB- rating on Guam’s general obligations, which is three steps below investment grade.

‘Substantial Savings’

Some tax-exempt bonds due in 2039 priced to yield 3.91 percent, or 0.88 percentage point more than benchmark munis, Bloomberg data show. By comparison, bonds with the same maturity sold in 2009 for 7.18 percent.

“They’re swapping one type of debt for another, and the overall leverage position of the government is unchanged,” said Paul Dyson, an S&P analyst in San Francisco. “Because of the rating differential, they’re generating substantial savings.”

The business-tax collections that will repay the bonds grew to about $238 million in the fiscal year that ended in September from $222 million during the period that ended 12 months earlier, offering documents show.

Calvo, a Republican, said in an interview that the taxes will grow with the island’s economy. Guam is reliant primarily on tourism and U.S. military operations.

Seeing Stability

Guam received a record 1.34 million tourists in 2014, with hotel taxes increasing by more than 50 percent since 2010, as it attracted more travelers from South Korea, Taiwan and the U.S., offering documents show.

That offset a decline from Japan, its biggest market, as the weakening of the yen against the dollar made the island more expensive, said Calvo, who plans trade missions to China, Taiwan and other southeast Asian countries.

“What we’ve done most importantly is brought stability,” Calvo said via telephone. “The fundamentals short-, mid- and long-term in Guam to me are nothing but promising, and that’s where maybe you have some differences” from Puerto Rico.

The 212-square-mile island, less than one-fifth the size of Rhode Island, still has its challenges. After two years of surpluses, which erased a $303 million general-fund deficit, Guam’s expenses exceeded revenue by about $60 million for the year that ended in September, offering documents show.

The U.S. military’s decision to scale-back a buildup on the island will restrain its growth. What was once projected to be a $15 billion boost to the Guam economy is now just $8 billion, S&P said.

“When you have a strong economy, you see more jobs, better paying jobs, and a community feels confident,” Calvo said. “We’ve got to continue to be fiscally prudent.”

The U.S. territory of Puerto Rico owes more than $70 billion—about $19,729.43 per resident—in debt to creditors and investors. First to note the territory’s fiscal problems were the credit rating agencies, which downgraded the territory’s bond status to “speculative,” the first of three steps along the junk-bond path to loan default.

Over the summer, about a year and a half after insiders warned of the territory’s looming problems, Gov. García Padilla (PPD) announced, “[T]he debt is not payable.”

“My administration is doing everything not to default,” Garcia Padilla said in an interview with TheNew York Times. “But we have to make the economy grow. If not, we will be in a death spiral.”

Some territory agencies, such as the Puerto Rico Electric Power Authority, are negotiating forbearance agreements with bondholders, but the future of most of the territory’s municipal debt continues to be up in the air.

Without major reforms, the crisis playing out in Puerto Rico will come home to roost in the mainland United States as well, as state governments continue to walk down the same financial path as Puerto Rico and Greece.

One of the root causes of Puerto Rico’s inability to pay its bills is the high cost of doing business in the territory. The litany of mandatory fringe benefits for employees—treated as bonuses elsewhere in the United States—discourages businesses from investing in the territory because the labor costs exceed employee productivity.

Stateside, the cumulative impact of countless business-unfriendly laws in California and New York has caused numerous businesses and the people employed by them to leave those states. Between 2013 and 2014, New York’s net population declined by 153,921, and the number of people leaving California exceeded new arrivals by 32,090. Like Puerto Rico, both California and New York are known for complex tax codes that distort the economy and discourage business investment.

The inevitable result of this incessant business-harassment is fiscal insolvency. Just like Puerto Rico before the fiscal tsunami hit, California carries a jaw-dropping amount of public debt. Adding in the cost of postponed payments to public schools and universities, deferred Medicaid entitlement payments, and other gimmicks, California taxpayers are on the hook for $443 billion in liabilities, or about $11,417.53 per resident.

The situation confronting New York taxpayers is only slightly less bleak than that of a Puerto Rican taxpayer. Each and every New York resident is on the hook for $18,222.78 in public debt. In response to such crushing amounts of public debt, politicians raise taxes even higher, which suppresses economic activity and resultant tax revenues even further, creating the “death spiral” predicted by Padilla.

Tax hikes chase away new business investment and encourage businesses to move. People then move to other states because of the lack of available jobs, and tax revenue falls short of expectations as employment rates and economic activity decline. The bills pile ever-higher as a result. The symptoms of the economic disease crippling Puerto Rico are already present in some states around the nation.

It may be too late for Puerto Rico, the “Island of Enchantment,” but similar high-tax, high-regulation states still have time to avert disaster if they stop treating taxpayers like ATMs and start enacting pro-taxpayer, pro-growth reforms. If they don’t change their ways soon, the result will not be enchantment, but fiscal ruin.

In August 2015, two municipal issuers tested the financial markets: The city of Detroit and the Puerto Rico government-owned Puerto Rico Aqueduct and Sewer Authority (PRASA). Detroit filed for bankruptcy in 2013, its bondholders taking deep discounts. PRASA has always met its credit obligations. Detroit easily placed its debt at 4.5 percent, while PRASA had difficulty in placing debt at more than 9 percent. Meanwhile, the government-owned Puerto Rico Electric Power Authority (PREPA) is shut out of the capital markets.

Chapter 9 of the U.S. Bankruptcy Code protects a political subdivision, public agency or instrumentality of a state. In 2013, Detroit filed for a debt restructuring under Chapter 9, which gave the city the possibilities for a new beginning. The results thus far are promising. The law applies to the 50 states, but not to Puerto Rico.

Congress has been unwilling to extend Chapter 9 protection to the territory. The result is difficult negotiations between bondholders demanding pounds of flesh and Puerto Rico government instrumentalities. Puerto Rico is unable to use the possibility of filing bankruptcy as leverage to reach reasonable agreements. Negotiations could drag on for a long time, becoming an impediment to Puerto Rico's economic recovery.

The negotiations between the bondholders and PREPA are a case in point. The bondholders shared a proposal with the press in July 2015 that would have a negative impact on the island because it would increase electricity rates. Given the present dire state of the Puerto Rico economy, such an increase would imply further economic contraction and continuing emigration.

According to bondholders, the electricity rate would decline from the 28 cents per kilowatt-hour a year ago, August 2014, to something in the vicinity of 24 cents per kilowatt-hour. However, this implies an increase from the present 21 cents per kilowatt-hour even if the bondholders' projections pan out. As stated by Stephen Spencer in a previous contribution to The Hill: "Our proposal would result in Puerto Rican electricity rates being roughly 15 percent lower than PREPA's 'status quo' rate. We used the average August 2014 electricity rate because this was when we started negotiations, so it's the benchmark we have been using throughout this process."

The July proposal also included Capital Appreciation Bonds (CAB). These involve no disbursement by PREPA over 20 years because even after the rate increase, cash flow would not be enough to pay these bonds. Therefore, the bonds would accrue interest over 20 years at S&P AAA Municipal Bond Yield plus 200 basis points. Then, starting in 2035, somehow, PREPA and its Puerto Rico clients are supposed to come up with more than $5 billion.

Detroit was able to spread out the pain of debt restructuring among residents, pensioners, public-sector workers and bondholders. Today, Detroit is coming back as a city. Puerto Rico instrumentalities would be able to spread the pain if Chapter 9 was available to them. Even in the absence of Chapter 9, Puerto Rico should still strive to restructure debt in a fair way.

References to the disbursement of Capital Appreciation Bonds have been corrected.

Feliciano is an economist and president of Advantage Business Consulting.

Revelers arrived in cars sporting the American flag and wore clothes in red, white and blue as they celebrated the anniversary of Puerto Rico's pro-statehood political party with deafening salsa music and speeches.

Like many others worried about the U.S. territory's future, those rallying Thursday night in the coastal town of Manati believe that statehood can help pull it out of a nearly a decade of economic stagnation. "Puerto Rico has to become a state," insisted 63-year-old celebrant Norma Candelario.

With unemployment at 12 percent, and the public debt reaching $72 billion, advocates for making the Caribbean island the 51st state say the economic woes are strengthening their arguments. As a state, Puerto Rico's municipalities and public utilities would no longer be prohibited from restructuring their debts through bankruptcy. It would also receive more of certain kinds of federal funding that other states get.

"The crisis has made us more visible worldwide," said Carlos Pesquera, a former Puerto Rico transportation secretary who attended the rally. "I would have preferred that the crisis not happen, but we're going to take this as an opportunity to define our status, to see it as a solution."

Puerto Ricans have been divided over their relationship to the U.S. mainland for decades. Since 1967, most voters in three referendums have favored remaining a semi-autonomous territory, which advocates say preserves the island's cultural identity and provides more local control.

Statehood was a close second place in all three votes, with independence coming in a distant third. But support for joining the union rose in each referendum and appears to be gaining. In the most recent election, in November 2012, for the first time more than half of voters said they favored a change from the territory's current status and a plurality said they supported statehood. Backers of the status quo said the ballot was flawed and rejected the outcome.

A recent poll by local research firm Gaither International found 40 percent of Puerto Ricans favored statehood, with 27 percent opposed and 33 percent expressing no opinion. Among those with an opinion, 60 percent favored statehood, compared with 56 percent in a similar poll conducted five years ago.

"Puerto Rico needs statehood at some point because of the economic crisis," said Nel Balseiro, 43, a funeral home owner and former mayor who until two years ago supported the status quo. "We need that to have a real chance at progressing."

The gains for statehood reflect the dismal times on the island, said Gilberto Castro de Armas, managing director at Gaither International.

An estimated 144,000 people left the territory between 2010 and 2013 in the largest exodus in decades and about a third of all people born in Puerto Rico now live in the U.S. mainland. So many businesses and schools have closed and so many people have left the island that some neighborhoods resemble ghost towns.

"Political changes occur during times of economic and social stress," said Castro de Armas. "You don't have to be a fortune teller. People are abandoning the ship because they think it's sinking."

Statehood proponents say the exodus is the best proof of growing support for their cause.

Judith Colon, 44, who manages social media accounts for Puerto Rico's pro-statehood party, said moving to the U.S. is among the few options available to Puerto Ricans struggling economically.

She and other statehood supporters say joining the union would provide the kind of needed economic benefits Puerto Ricans get when they move to the mainland.

The local government receives lower Medicaid and Medicare reimbursements, forcing it to spend more than $1 billion a year in Medicaid alone than if it were a U.S. state, said island congressional representative Pedro Pierluisi, who is running for governor next year. Puerto Rico also faces limited child tax credits and is barred from accessing other tax credits including one meant to promote labor participation, and there is no supplemental Social Security income for disabled people, he said. In addition, there's a cap on a nutritional assistance program in which the island is shortchanged by roughly $1 billion a year, he said.

"The current crisis has brought to light the limits of Puerto Rico's current territorial status," said Pierluisi, who promises to hold a referendum on whether the island should become a state if he's elected. "From an economic standpoint, there's no question that billions of additional dollars would be flowing into Puerto Rico's economy if we were treated equally and fairly ... The disparities we have in the way federal programs apply in Puerto Rico are atrocious."

Statehood supporters also say joining the union would end their perceived second-class status. Even though Puerto Rico residents are U.S. citizens, they cannot vote in the presidential election and have only one representative in Congress who has limited voting power.

But the island's Gov. Alejandro Garcia Padilla, whose party supports the current commonwealth status, has said statehood "would turn Puerto Rico into a ghetto."

Others, like Jorge Colberg, secretary of Garcia's Popular Democratic Party, say Puerto Rico's economic problems are a result of poor public administration, not its status. "Spending more than what you have has nothing to do with political status," Colberg said.

He said that holding a plebiscite now would create uncertainty for investors as the island tries to restructure its debt and warned that statehood would eliminate certain tax breaks and increase other taxes.

Puerto Rico statehood would require approval from Congress, where it would face a tough fight because the territory is considered to lean Democratic and it would have two senators and five representatives if it became a state. But it could be hard for Congress to block it if a strong majority of Puerto Ricans demonstrated support for joining the union.

President Barack Obama has said he supports statehood if Puerto Ricans clearly back it, and Republican presidential candidate Jeb Bush has said he believes statehood is the best option.

Many on the island think Puerto Rico is nearing that day.

"This is the best inheritance we can leave our children," said Candelario, who moved back to the island from the Bronx to help out a struggling daughter. "I have grandchildren, and I would like to leave them something special. It would be good if they could study here and work here."

On Monday, August 3, Puerto Rico’s Public Finance Corporation defaulted on a $58 million USD bond payment, the island’s first debt nonpayment in its 117 years as a U.S. territory. Puerto Rican Governor Alejandro García Padilla has called the $72 billion USD debt “not payable.”

A report by former IMF economist Anne Krueger sponsored by the Government Development Bank of Puerto Rico offered a neoliberal analysis of the situation. To Krueger, Puerto Rico’s problems stem from the commonwealth’s too high minimum wage and overly generous welfare benefits.[1] A somewhat less reticent report sponsored by a group of hedge fund managers, who control a significant chunk of Puerto Rican debt, recommended outright austerity measures such as making sharp cuts to education and health care.[2]

However, these neoliberal prescriptions are far from offering a viable solution to Puerto Rico’s current troubles, which actually grow out of more complex, long-term causes, especially the island’s lack of autonomy in constructing its own economic policies. Puerto Rico’s relationship with the United States continues to be one of colonial-style dependency, serving to assure the overwhelming influence of powerful U.S. economic interests. The twentieth-century colonial policies, which allowed corporations to extract wealth from the island through foreign ownership of land and other productive property, have helped pave the way for a new chapter in the history of colonialism, characterized by exploitative debt obligations which largely benefit Wall Street.

A Colonial History: The Role of U.S. Capital

Puerto Rico became a North American colonial experiment when the Spanish-American War ended the island’s eight days of independence in July 1898. Since then, Puerto Rico has been steadily transformed into a reserve for U.S. capital. The process got a boost in 1899 when Hurricane San Ciriaco destroyed the island’s farmlands at a time when coffee was the principle export. U.S. banks swooped in and began to loan money to impacted coffee farmers, but, in lieu of any usury laws, extortionate interest rates led to mass defaults and farm foreclosures.[3] As the coffee sector fell into steep decline, sugar, a capital-intensive crop, became the dominant export by 1901, transforming Puerto Rico into a one-crop economy selling almost exclusively to the United States. By 1930, 41 out of 146 sugar mills produced 97 percent of the output, and 11 of the 41 were owned by four U.S. corporations which held over half of Puerto Rico’s arable land. Between 1927 and 1928, these four companies produced over 51 percent of the island’s sugar, with the United States dominating the industry and, in turn, the majority of the island’s wealth.[4]

Modern U.S. capital has taken several steps to ensure its domination of the territory’s wealth. The infamous Jones Act of 1917 still requires that all goods shipped into or out of Puerto Rico be carried on U.S. vessels, often doubling the price of imports.[5] Moreover, Puerto Rico’s notorious tax policies, including the Revenue Act of 1921, have turned the island into a corporate haven. In 1976, the creation of IRS Section 936 tax code enhanced the tax breaks that U.S. corporations enjoyed.[6] To promote investment, the law allowed U.S. companies to operate in Puerto Rico without paying corporate taxes at all, attracting especially pharmaceutical companies.

Initially, the 1976 provision was successful in making the commonwealth a hub for U.S. investment and pharmaceutical manufacturing.[7] However, in 2006 the tax break expired, setting off a recession that has helped fuel the current debt crisis. Companies deserted the island in droves, causing employment to fall 10 percentage points between 2006 and 2010, and an emigrating labor force drained the island’s tax base.[8]

As the Center for the New Economy points out, in Puerto Rico today “both production and consumption are dominated by the foreign sector,” and, therefore, “most of the income derived from the manufacturing and sale of exports accrues to and is repatriated by absentee owners, with little impact on the local economy.”[9] In addition, Jacobin Magazine notes that, “a substantial amount of wealth created in the island is extracted and not reinvested,” and about one-third of the island’s GNP is “repatriated back to the U.S.”[10] Meanwhile, Puerto Rico has turned to regressive imposts to gather revenue, with its sales tax two percentage points higher than that in Tennessee, the state with the next highest rate. This is a particularly harsh impost on the poor, given that the island’s GNP is less than half that of Mississippi, the mainland’s poorest state.[11]

A Neo-Colonial Present: The Role of U.S. Vultures

Due to the tax breaks on U.S. subsidiaries in contrast to the island’s high domestic corporate tax rates, Puerto Rico never had the opportunity to develop its internal private sector. As a result, when Section 936 expired, the government became the island’s largest employer but found itself in desperate need of investment to fund its projects.[12]

The solution came in 2012 in the form of two laws passed under the conservative administration of Governor Luis Fortuño, which continue to be implemented during the present administration of the more moderate Governor García Padilla. The laws provide new tax incentives to wealthy investors. [13] One, the Export Services Act, offers hedge funds a low 4 percent tax rate, and the other, the Individual Investors Act, provides investors 100 percent tax exemptions on all dividends, interest, and capital gains on the condition that the investor lived on the island for half a year.[14]

The two new tax breaks immediately drew in hordes of wealthy investors, enticed by the chance to buy up triple-tax exempt bonds from the public sector. Government bonds initially drew in mutual funds, which rely more on the economy’s performance, but for the past year they have been traded in secondary markets at lower levels, attracting hedge and vulture funds with no authentic interest in the island’s economic development.[15] Vulture funds, the speculative, more extreme subcategory of hedge funds, are particularly drawn to countries that are predicted to be facing economic crises and possible default. These investors buy high-risk distressed bonds for pennies on the dollar, only to later demand full repayment of the debt, walking away with billions in winnings. One such predator is DoubleLine Capital’s Jeffrey Gundlach, who profited off of the housing crisis in 2008 by buying distressed municipal bonds as the U.S. economy fell into recession. Gundlach, comparing the crisis on the mainland to the one in Puerto Rico, encouraged investors to begin buying the territory’s bonds in May when they fell to about 78 cents on the dollar, according to Bloomberg Business.[16]

CNN Money reports that hedge funds currently hold about $15 billion USD of Puerto Rico’s $72 billion USD debt, while the Puerto Rico-based Centro del Periodismo Investigativo (Center for Investigative Journalism; CPI) estimates that hedge and vulture funds together may hold up to 50 percent of the debt. One can be certain that these investors will keep close watch over any payment plan or debt restructuring in order to guarantee themselves a substantial profit.[17] Indeed, hedge and vulture funds have already begun lobbying against any measure that would enhance the Puerto Rican government’s autonomy to seek a measured plan for handling its growing debt.

Unable to declare Chapter 9 bankruptcy due to the island’s territorial status, García Padilla enacted a debt-restructuring law called the Puerto Rico Public Corporations Debt Enforcement and Recovery Act. The law resembled bankruptcy, as it sought some level of protection from bondholders; it claimed to be a “solution to ensure that vital public services such as the delivery of electricity, gas and clean water are not interrupted in the short-term” and proposed negotiations between the public corporations and their creditors.[18] However, a group of investors, who at the time held about $2 billion USD of the Puerto Rico Electric Power Authority’s debt, sued the commonwealth in federal court, claiming that the law would interfere with their contractual rights. In February, the court struck the recovery act down as unconstitutional.[19]

A similar situation began almost a decade ago in the case of vulture funds in Argentina, when the South American nation defaulted twice on its massive debt. When President Cristina Fernández de Kirchner’s administration defaulted again in 2012, a group of vulture funds led by billionaire investor Paul Singer sued the Argentinian government in New York’s South District Court, refusing to accept the debt restructuring. One of the principle hedge funds involved in the lawsuit, Aurelius Capital, also currently holds a portion of Puerto Rico’s debt, according to a report by CPI.[20] The court ruled in favor of the vultures, and the Argentinian economy remains deeply troubled as the government is forced to make 100 percent repayments for bonds that were bought at a fraction of the price.[21] While the U.S. government argued in favor of Argentina, the Obama Administration refrained from taking any concrete action in attempting to relieve the crisis, even though, as The Guardian noted, Obama could have adjourned Singer’s lawsuit simply by telling the district court that it “interferes with the president’s sole authority to conduct foreign policy.”[22]

Perhaps Obama’s inaction was in part due to the immense lobbying power of hedge fund managers like Singer, one of the most influential contributors to Republican candidates.[23] There are similar lobbyists on the Democratic side, such as Robert Raben, former Assistant Attorney General under President Clinton and the executive director of a group called the American Task Force Argentina (AFTA), which represents the vulture funds suing Argentina. Raben’s influential lobbying firm has received over $2 million USD from AFTA, and the latter “has spent nearly $4 million lobbying the White House, Treasury Department and U.S. Congress.”[24] These relationships reveal an unsettling truth: The forces of big capital often override a U.S. policymaker’s principles of sovereign rights and fair diplomacy. A similar relationship between policy and capital has driven the crisis in Puerto Rico. As the CPI report notes, the “hedge and vulture fund representatives visit the offices of legislators at the Capitol constantly.”[25]

Conclusion

Puerto Rico’s confrontation with vulture funds may not reach the same impasse as in Argentina. Indeed, Washington might even have some incentive to protect the territory from what Governor García Padilla has called a “death spiral,” as a complete collapse of the economy would render this colonial experiment a failure in the eyes of the Hemisphere. However, even if the commonwealth were granted Chapter 9 rights, Puerto Rico would remain bound by the chains of dependency. The crisis in Puerto Rico is a result of dubious policy decisions by the Puerto Rican government and Washington. United States’ colonial policies imposed on the island throughout the past century have turned Puerto Rico into a haven for cheap manufacturing. No amount of micromanagement of the ailing economy, by the IMF or by independent hedge fund managers, can cure Puerto Rico’s colonial crisis. Until Puerto Rico enjoys the right to shape its own economic policies, it will continue to suffer the predations of largely unregulated, U.S. capital. And the vultures will continue to circle.

*Emma Scully, Research Associate at the Council on Hemispheric Affairs

Puerto Rico's FDIC-insured banks are well capitalized but the Federal Deposit Insurance Corp stands ready to act if one should become insolvent, according to a letter sent to Congressman Sean Duffy, chairman of a Financial Services subcommittee who had inquired about their health.

Puerto Rico's Governor Alejandro Garcia Padilla shocked investors in June when he said the island's debt, totaling $72 billion, was unpayable and required restructuring. The island has been in recession for nearly a decade.

"Our committee has jurisdiction over banks ... and we have been working on the safety and soundness concerns of Puerto Rico banks," said Duffy, who is separately working on a proposal to look for solutions to Puerto Rico's problems with possible ideas including using a financial control board.

Duffy requested in an Aug. 4 letter that the U.S. regulator detail how it was addressing potential issues among the island's banks.

The FDIC is "closely monitoring the fiscal and economic situation in Puerto Rico and assessing the potential impact on individual institutions," said an Aug. 18 letter from FDIC chairman Martin Gruenberg, provided by Duffy's office. The FDIC confirmed its authenticity.

Beginning in September 2013, the FDIC held regular discussions with the banks it supervises about their holdings of Puerto Rico debt and "observed a decline in the exposure over time."

The five FDIC-insured Puerto Rico banks - Banco Popular de Puerto Rico, Banco Santander Puerto Rico, FirstBank Puerto Rico, Oriental Bank and Scotiabank de Puerto Rico - had $442 million exposure to Puerto Rico government securities in September 2013. That fell to $240 million as of June 30.

The banks are well capitalized, the letter said, and the FDIC stands ready to "ensure the orderly, least costly resolution of failed insured depository institutions should one of them become insolvent."

Duffy, a Republican from Wisconsin, also said he is working on broader ideas for a draft proposal to address solutions for Puerto Rico.

Ideas could include a financial control board, an idea proposed in June by Republican Congressman Jeffrey Duncan, and Duffy is examining the possible impact of lifting the Jones shipping Act.

The Jones Act requires ships carrying goods from one U.S. port to another to be built in the United States.

He did not rule out supporting extending Chapter 9 bankruptcy protection for Puerto Rico entities, currently a Democrat-supported proposal, but would like to see it part of wider reforms.

"We have to come up with solutions that help the Puerto Rico people," said Duffy. "It's incumbent upon Republicans to engage on this issue."

(Adds quote from professor, background about likelihood of getting a case heard by Supreme Court)

NEW YORK Aug 21 (Reuters) - Puerto Rico on Friday asked the U.S. Supreme Court to overturn a ruling that blocks the restructuring of the commonwealth's public agencies, as the island grapples with trying to restructure its huge debt load.

In a petition seeking the court's review, which was provided by one of the island's lawyers, Puerto Rico said a lower court erred in concluding that U.S. bankruptcy law blocks the restructuring of the agencies' debts.

Puerto Rico also said the lower court decision leaves its public utilities in a legal "no man's land" because neither federal law nor the island's own law permits the needed restructuring.

"That decision leaves Puerto Rico's public utilities, and the 3.5 million American citizens who depend on them, at the mercy of their creditors," the commonwealth said. "This court's review is warranted - and soon."

Puerto Rico's Governor Alejandro Garcia Padilla shocked investors in June when he said the island's debt, totaling $72 billion, was unpayable and required restructuring. The island has been in recession for nearly a decade.

Puerto Rico passed the so-called Recovery Act last year to give certain public corporations, with around $20 billion in debt, the ability to restructure financially in an orderly process.

That was struck down by a federal court in Puerto Rico in February after bondholders in the island's power authority, argued in a lawsuit that the legislation contravened the U.S. bankruptcy code, which expressly excludes Puerto Rico. A U.S. appeals court in July affirmed the lower court decision.

A separate effort is underway in Congress to gain support for extending U.S. Chapter 9 to Puerto Rico entities.

"The basic question is whether Congress can say to the states that Chapter 9 is the only way to restructure municipal debt," said Stephen Lubben, a bankruptcy expert and law professor at Seton Hall university school of law. "Trouble is, Puerto Rico, which is not a full fledged state, has had trouble getting the courts to focus on that issue."

The Supreme Court typically hears arguments in only about 70 to 75 of the thousands of cases it is asked each year to consider, most often when lower courts are divided on an issue.

Puerto Rico said no such split is realistically possible in its case given its "anomalous treatment" under U.S. bankruptcy law. But it said the court should step in as the island tries to arrest a "financial meltdown" that threatens its future. (Reporting by Megan Davies and Jonathan Stempel; additional reporting by Nick Brown in San Juan; editing by Bernard Orr)

Sitting at a table in the airy ground floor headquarters of Beta Local, a nonprofit contemporary art space in Old San Juan, its co-director Pablo Guardiola lays out the organization's financial straits in stark terms. “We’ve experienced a major drop in membership,” he says. When Beta Local was founded in 2009, it had 10 primary members who paid $2,000 a year in dues. By now, Guardiola had hoped to have 30 such members, but with Puerto Rico’s uncertain financial future, donors are few and far between. “Today,” Guardiola says, “I think we just have three.”

When Puerto Rico defaulted on a debt payment on Aug. 3, it was the culmination of a harsh reality that arts organizations on the island had been grappling with for several years. “We had more than 400 employees in 2010,” says Jorge Irizarry Vizcarrondo, executive director of the Institute of Puerto Rican Culture. “We’re close to 150 now.”

Cuts to Public Funding

Irizarry Vizcarrondo’s organization is funded by Puerto Rico’s state government and the National Endowment for the Arts and manages, among other things, 12 museums across the island, 32 cultural centers, several theater festivals, and a handful of local art fairs. Two years ago, the Institute of Culture’s budget was close to $12 million, Irizarry Vizcarrondo says. Today, it has shrunk close to 26 percent, to $8.9 million. Of that amount, $1.5 million is automatically deducted for maintenance and utility payments, he says, and another $5.2 million is set aside for payroll, leaving just $2.3 million for programming for the entire island. (For context, the Metropolitan Museum of Art has a yearly operating budget of more than $300 million.)

The entrance of the Museo de Arte de Puerto Rico in San Juan.

Photographer: Christian Science Monitor/Getty

All that adds up to a vastly diminished state-sponsored cultural environment across the entire island. “The reduction in budget has seriously affected us,” says Irizarry Vizcarrondo. “We have services we’re mandated by law to provide, but we’ve reduced the support we give other arts organizations and cultural centers.” A theater festival, for example, used to receive between $30,000 and $40,000, he says. Now it gets $15,000 to $20,000.

Endangered National Identity

The cuts to Puerto Rico’s cultural organizations are particularly problematic, because “we’re not a nation state, we’re a cultural nation,” says Carla Acevedo-Yates, a Puerto Rico-based curator and writer. National identity comes from the distinctive Puerto Rican culture, in other words. Arts organizations are a big part of that. “Culture has always been instrumentalized as a nation building tool," Acevedo-Yates says.

But while large, state-supported museums are struggling, Acevedo-Yates observes that the small, artist-run spaces that dot Santurce, an up-and-coming neighborhood in San Juan, are still functioning as they always did. “The crisis has engendered a need for collaboration and support," she says. Last week, for instance, an event was held at the space La Productora to raise funds for the Puerto Rican artist Jotham Malavé Maldonado. "It was full of people, everyone pitching in 10 or 15 bucks so he could go to the Florence Biennial," Acevedo-Yates says.

Alternative Funding Structures

Beta Local, the nonprofit in Old San Juan, has an annual operating budget of around $140,000 and is too large to rely solely on the largess of the community, says Guardiola. As money has dried up, “we’ve developed a whole new strategy,” he explains. They’ve begun an aggressive grant-application campaign, and last year the organization was awarded a significant, two-year-long grant from the U.S.-based Warhol Foundation. “We’ve lost money from members, but now we’re getting it from other sources,” he says.

Irizarry Vizcarrondo is also looking into alternative funding structures for the Institute of Puerto Rican Culture, specifically from corporate and major individual donations. Even so, “we’re looking at this as a crisis that we’ll come out of,” he says. “I don’t think what we’re doing can be sustainable for another three or four years.”

Puerto Rico’s debt is more than triple what Detroit’s was two years ago when that city was forced into bankruptcy. The island territory, however, doesn’t have that option.

The economic troubles, coupled with crime and drought, have forced many people to move to the mainland United States in search of opportunity.

Here & Now’s Jeremy Hobson talks with 27-year-old Emmanuel Carasquillo about his decision to leave the island last year.

Earlier this year, social work student Coraly León arrived at her research assistant job at the University of Puerto Rico to find her salary abruptly cut in half due to budget cuts. “Not only do I have to find another job in order to support myself,” she told ThinkProgress, “but I still have to somehow complete my required 25 volunteer hours a week in order to graduate, on top of my research assistant work, on top of studying, on top of being an activist. I really don’t know if I can go on like this.”

León has managed, in a diminished capacity, to continue her research comparing the social work models of Cuba, the Dominican Republic and Puerto Rico. But one friend in her program, after losing her research funding, had to drop out and return to her family’s village. León worries many more could follow, like her friend Neftalí Sánchez Cordero who told ThinkProgress: “I depend on aid from the university. I work as a TA for 15 hours a week in order to pay my costs inside and outside of school. If I lose this work, I can’t continue my studies.”

The U.S. commonwealth of Puerto Rico is currently facing a$72 billion debt crisisfueled by Wall Street vulture funds, corruption, and wasteful spending. Now, the austerity the government has imposed to deal with the crisis has hit students especially hard. Deep, repeated cuts to public education have come at a time when the island already spendsless per studentthan most states, and more than45 percentof the population live in poverty.

The island’s hedge fund creditors aredemanding further austerity, including firing more teachers, closing schools, and further cutting the budget of the University of Puerto Rico.

“Every year, a degree is a less accessible, especially for working-class families,” León said. “The university is about to make a substantial cut to its budget, which is going to dismantle the services we need as students. That’s coming at the same time the cost of living is going up — food, housing, transportation, books — everything we need to survive.”

A poster at the University of Puerto Rico in San Juan reads, “Here we need more professors. Take back the UPR!”

CREDIT: ALICE OLLSTEIN

Aaron Gamaliel Ramos, a professor of Caribbean Studies at the University of Puerto Rico, bristles at the thought of U.S. hedge funds demanding cuts to his university.

“Education is so important that it should be free,” he told ThinkProgress. “It’s not a waste of money, it’s an investment in the future of the country.”

Ramos feels that Puerto Rico is trapped in a “clash of visions” between Latin America, where higher education has historically been free, and the U.S., where most students graduatedeep in debtand professors have to scramble for research funds. Though tuition is much lower at the University of Puerto Rico than most U.S. universities, it’s high enough that92 percentof students depend on financial aid, including Pell Grants, federal loans, and work-study programs.

“Inmyvision, students who are poor who meet the requirements shouldn’t have to pay a cent,” said Ramos. “Those who come from families with money should pay something, but everyone should be supported.”

To pay for this vision, he proposed raising taxes on foreign corporations and wealthy investors, who currently use the island asa tax haven.

But instead of taxing corporate profits, the struggling Puerto Rican government decided to implement policies that disproportionately target the poor. In July, they raised the sales tax to 11.5 percent — thehighest rateof all U.S. states and territories. The country is also on the verge of raisingthe price of tap waterin the middle of abrutal drought— in order to please its hedge fund bond holders.

Deep cuts have hit public transportation as well, and in San Juan some buses no longer run on certain days. Fares have climbed to 75 cents per ride, a burden for many of the island’s working poor and unemployed. For students who drive, like Francisco Santiago, ahike in the gas taxhas made everything from getting to class to visiting his family in Guayama much more difficult.

“This is part of the whole neo-liberal model that’s being imposed on Puerto Rico: cutting social services from the people little by little,” he told ThinkProgress. “We have this debt, but not everyone is paying it. The poorest class is the one paying, and the middle class. Since our quality of life is getting worse, we have to fight not just for ourselves but for future generations of students.”

Student Coraly León walks by graffiti that reads, “Look into my unemployed face.”

CREDIT: ALICE OLLSTEIN

As the debt crisis worsens, the president of the University of Puerto Rico recentlyreassured local press: “The University is serving the country well, and you can see the evidence of that every day.”

But the students who spoke to ThinkProgress shared concerns that this may not be true if austerity continues. That’s why they held a48-hour strikein May to protest the budget cuts, tuition hikes, and threats to the retirement benefits of faculty and staff. More and more, they see their fellow studentsgraduating with debtinto a job market with12 percentunemployment. With their governmentdefaultingon its debt and projecting its cash to dry up by this November, the students are calling on their U.S. mainland counterparts to stand with them in solidarity.

“The problems that workers, students and the poor are facing in the U.S. are the same that we face here in Puerto Rico: access to education for the poor and working-class,” Enrique Fortuño told ThinkProgress. “My message is that our fight is the same fight. In some cases, we’re even fighting the same people, the same multinational companies and banks who are exploiting us.”

Fortuño wants U.S. students to pressure Congress to approvea billthat would allow the island to restructure its crushing debt. Yet the Republican-controlled Congress has not shown any willingness to pass — or even take up — the bill. Puerto Rico’s sole member of Congress Pedro Pierluisi introduced the measure this year, but cannot vote on it even though he represents more than 3 million U.S. citizens.

“We can’t declare bankruptcy, but we also can’t get bailed out,” lamented León. “So we’re stuck in limbo, where our hands are tied and we can’t do anything.”

CREDIT: Alice Ollstein

Student activists at the University of Puerto Rico stand by a portrait of Antonia Martínez -- a student killed by police in 1970 while protesting the Vietnam War